When to Enroll in Medicare — Complete Timeline 2026

When to enroll in Medicare is one of the most important decisions you will make as you approach age 65. Missing your Medicare enrollment window can result in permanent late penalties that increase your premiums for life. Understanding exactly when to enroll in Medicare — and which enrollment period applies to your situation — is critical to avoiding costly mistakes. In this complete 2026 guide we explain everything you need to know about when to enroll in Medicare including every enrollment period, every deadline, and exactly what happens if you miss your window to enroll in Medicare. All information is sourced from Medicare.gov and SSA.gov.

Also Read – How Does Medicare Work for Seniors — Complete Guide 2026

What You Will Learn — When to Enroll in Medicare

- When to enroll in Medicare for the first time

- The Medicare Initial Enrollment Period explained

- When to enroll in Medicare if you are still working at 65

- When to enroll in Medicare Part A vs Part B

- When to enroll in Medicare Part D drug coverage

- The Medicare Annual Open Enrollment Period

- Medicare Special Enrollment Periods explained

- What happens if you miss your window to enroll in Medicare

- The Medicare late enrollment penalty explained

- Frequently asked questions about when to enroll in Medicare

When to Enroll in Medicare — The Most Important Rule

The single most important rule about when to enroll in Medicare is this — enroll during your Initial Enrollment Period unless you have qualifying coverage from a current employer. Missing your Initial Enrollment Period without qualifying coverage results in permanent late enrollment penalties that stay with you for life.

When to enroll in Medicare depends on your specific situation. There are several different Medicare enrollment periods and knowing which one applies to you is the key to enrolling on time and avoiding penalties.

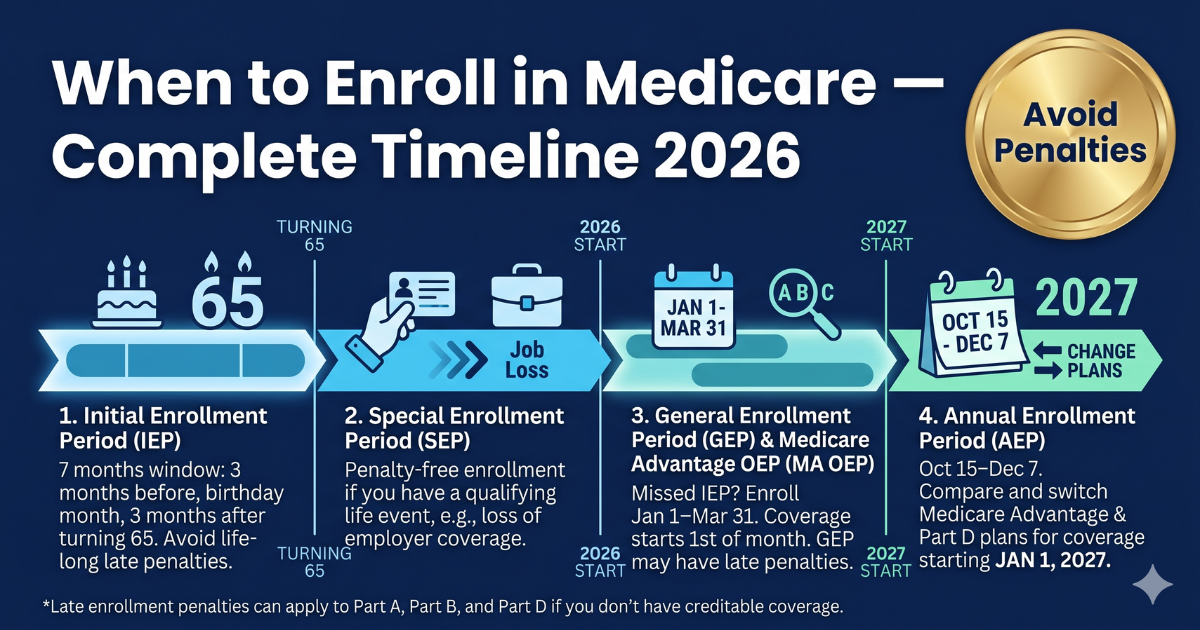

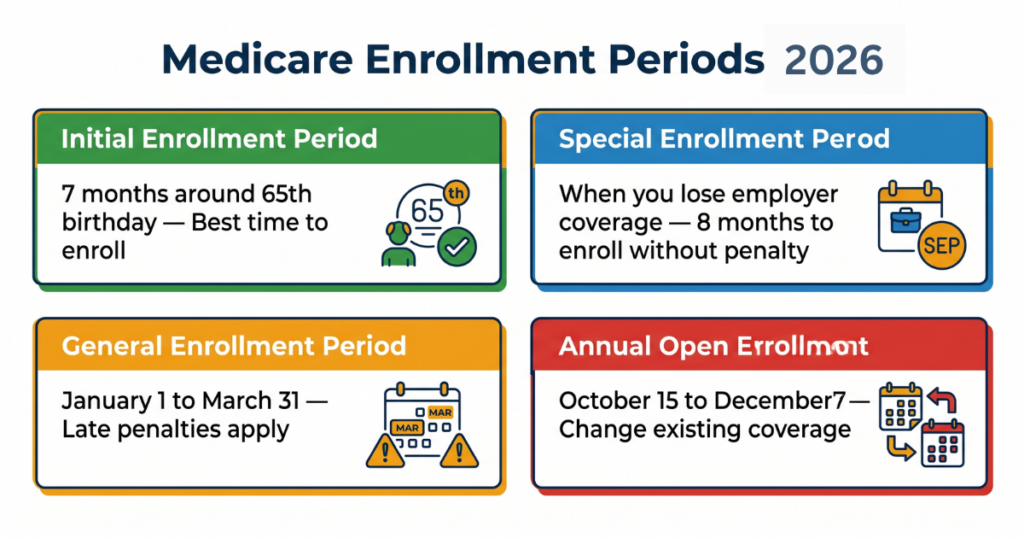

The five main Medicare enrollment periods that determine when to enroll in Medicare are:

- Initial Enrollment Period (IEP) — when most people first enroll in Medicare

- Special Enrollment Period (SEP) — for people with employer coverage

- General Enrollment Period (GEP) — for people who missed their IEP

- Annual Open Enrollment Period (OEP) — for changing existing Medicare coverage

- Medicare Advantage Open Enrollment Period — for switching Advantage plans

When to Enroll in Medicare — Initial Enrollment Period

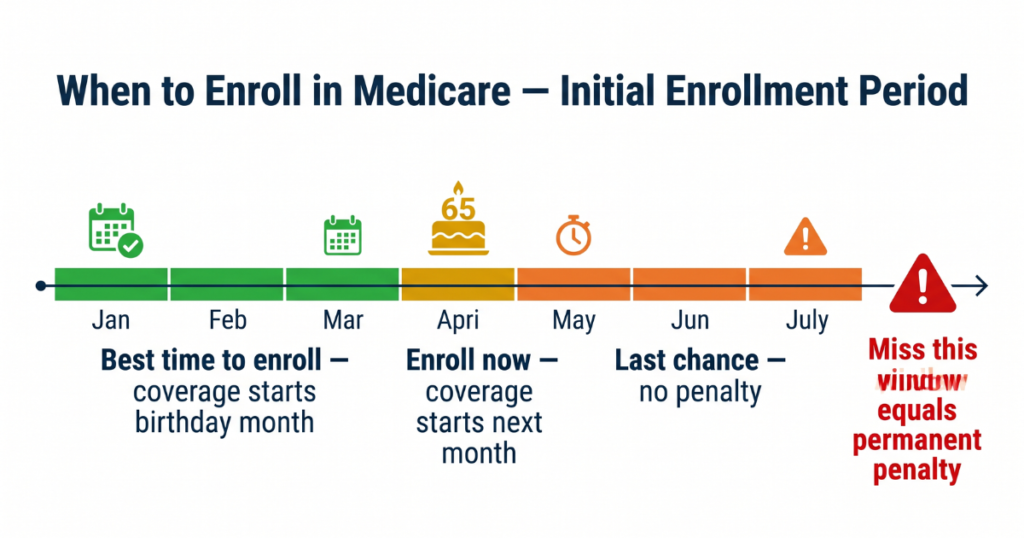

The Medicare Initial Enrollment Period is the primary window for when to enroll in Medicare for the first time. The Initial Enrollment Period is a 7-month window that begins 3 months before the month you turn 65.

Here is exactly when to enroll in Medicare during your Initial Enrollment Period:

- 3 months before your 65th birthday month — enrollment opens

- Your 65th birthday month — enrollment continues

- 3 months after your 65th birthday month — enrollment closes

For example if your birthday is July 15 your Initial Enrollment Period for Medicare runs from April 1 through October 31. This is your primary window for when to enroll in Medicare.

When to enroll in Medicare matters within the Initial Enrollment Period because your coverage start date depends on when you sign up:

If you enroll in Medicare during the 3 months before your birthday month your coverage starts the first day of your birthday month.

If you enroll in Medicare during your birthday month your coverage starts the first day of the following month.

If you enroll in Medicare during the first month after your birthday month your coverage starts the first day of the second month after you enroll.

If you enroll in Medicare during the second or third month after your birthday month your coverage starts the first day of the third month after you enroll.

The best time to enroll in Medicare within your Initial Enrollment Period is during the 3 months before your birthday month. This gives you the earliest possible coverage start date.

When to Enroll in Medicare Part A

For most people the answer to when to enroll in Medicare Part A is — as soon as you are eligible. Here is why:

Most people qualify for premium-free Medicare Part A. If you or your spouse worked and paid Medicare taxes for at least 10 years (40 quarters) you owe nothing for Part A coverage. Since Part A is free for most people there is almost never a reason to delay enrolling in Medicare Part A.

You can enroll in Medicare Part A without enrolling in Part B. Some people choose to enroll in Medicare Part A at 65 while delaying Part B if they have employer coverage. This is perfectly acceptable and there is no penalty for taking Part A while delaying Part B when you have qualifying employer coverage.

When to enroll in Medicare Part A if you are still working — enroll in Part A at 65 regardless. Since it is free there is no downside. Part A can coordinate with your employer insurance to cover hospital costs.

When to Enroll in Medicare Part B

Knowing when to enroll in Medicare Part B is more complex than Part A because Part B has a monthly premium and a late enrollment penalty. The answer to when to enroll in Medicare Part B depends entirely on whether you have other qualifying health coverage.

When to enroll in Medicare Part B if you are not working — enroll during your Initial Enrollment Period. If you are not covered by employer group health insurance when you turn 65 you must enroll in Medicare Part B during your Initial Enrollment Period to avoid the permanent late enrollment penalty.

When to enroll in Medicare Part B if you are still working — you can delay Medicare Part B enrollment without penalty as long as you are covered by employer group health insurance through your own or your spouse’s current employment. This is an important distinction — COBRA coverage, retiree health coverage, and VA benefits do not qualify as coverage that lets you delay Medicare Part B enrollment without penalty.

When to enroll in Medicare Part B after employer coverage ends — you have a Special Enrollment Period of 8 months starting the month your employer coverage ends or the month your employment ends — whichever comes first. You must enroll in Medicare Part B within this 8-month Special Enrollment Period to avoid the late enrollment penalty.

When to Enroll in Medicare if You Are Still Working at 65

One of the most common questions about when to enroll in Medicare is what to do if you are still working at 65 and covered by employer insurance. Here is the exact answer:

When to enroll in Medicare Part A at 65 while still working — enroll immediately. Part A is free for most people and there is no reason to delay. Part A can coordinate with your employer insurance.

When to enroll in Medicare Part B at 65 while still working — you can delay Part B without penalty as long as your employer has 20 or more employees and you are covered by the employer’s active group health plan. If your employer has fewer than 20 employees Medicare becomes your primary insurance and you should enroll in Part B immediately.

When to enroll in Medicare after you retire — you have an 8-month Special Enrollment Period after your employer coverage ends to enroll in Medicare Part B without penalty. Do not wait — the Special Enrollment Period starts when your employment or employer coverage ends, whichever comes first.

Important — do not confuse when to enroll in Medicare with when to enroll in Medicare Advantage or a Medigap plan. You must be enrolled in Medicare Parts A and B before you can enroll in Medicare Advantage or purchase a Medigap supplement plan.

When to Enroll in Medicare Part D Drug Coverage

When to enroll in Medicare Part D drug coverage follows the same basic rules as Part B enrollment. Here is when to enroll in Medicare Part D:

Enroll in Medicare Part D when you first become eligible for Medicare. The best time to enroll in Medicare Part D is during your Initial Enrollment Period — the same 7-month window around your 65th birthday.

You can delay Medicare Part D enrollment without penalty only if you have other qualifying drug coverage such as coverage from a current employer or union health plan. Your employer’s plan must be at least as good as Medicare Part D drug coverage — called creditable coverage. Your employer must provide you with a notice of creditable coverage each year.

When to enroll in Medicare Part D after losing qualifying coverage — you have 63 days from the date your other drug coverage ends to enroll in Medicare Part D without facing the late enrollment penalty. Do not miss this 63-day window.

When to Enroll in Medicare — Special Enrollment Periods

Special Enrollment Periods determine when to enroll in Medicare outside of the standard enrollment windows. Special Enrollment Periods allow you to enroll in or change Medicare coverage when you experience certain qualifying life events.

The most important Special Enrollment Periods and when to enroll in Medicare during each:

Losing employer coverage — you have 8 months to enroll in Medicare Part B and 63 days to enroll in Medicare Part D after losing employer health coverage.

Moving to a new service area — if you move outside your Medicare Advantage or Part D plan’s service area you have a Special Enrollment Period to switch plans.

Your plan leaves Medicare — if your Medicare Advantage or Part D plan stops participating in Medicare you have a Special Enrollment Period to choose new coverage.

Qualifying for Extra Help — if you qualify for the Low Income Subsidy for Medicare Part D you have a Special Enrollment Period to enroll in or change your Part D plan.

Moving into or out of a nursing facility — triggers a Special Enrollment Period for Medicare Advantage and Part D plans.

When to Enroll in Medicare — Annual Open Enrollment Period

The Medicare Annual Open Enrollment Period runs every year from October 15 to December 7. This is when to enroll in Medicare Advantage or Part D plans or make changes to existing coverage. Changes made during Open Enrollment take effect January 1 of the following year.

During the Annual Open Enrollment Period you can enroll in Medicare for the first time if you missed your Initial Enrollment Period and are using the General Enrollment Period. You can also switch from Original Medicare to Medicare Advantage, switch from Medicare Advantage back to Original Medicare, change from one Medicare Advantage plan to another, add drop or switch your Medicare Part D drug plan, and switch from one Part D plan to another.

When to enroll in Medicare during Open Enrollment — the earlier the better. Plans can fill up and early enrollment gives you more time to review your coverage decisions.

When to Enroll in Medicare — General Enrollment Period

The Medicare General Enrollment Period runs from January 1 to March 31 each year. This is when to enroll in Medicare if you missed your Initial Enrollment Period and do not qualify for a Special Enrollment Period.

If you enroll in Medicare during the General Enrollment Period your coverage starts July 1 of that year. You will also face late enrollment penalties for the months you went without Medicare coverage.

The General Enrollment Period is a last resort option — not an ideal time to enroll in Medicare. Always try to enroll during your Initial Enrollment Period or a qualifying Special Enrollment Period to avoid penalties and delays.

What Happens If You Miss Your Window to Enroll in Medicare

Missing your window to enroll in Medicare without qualifying coverage results in permanent late enrollment penalties. Here is exactly what happens when you miss your Medicare enrollment window:

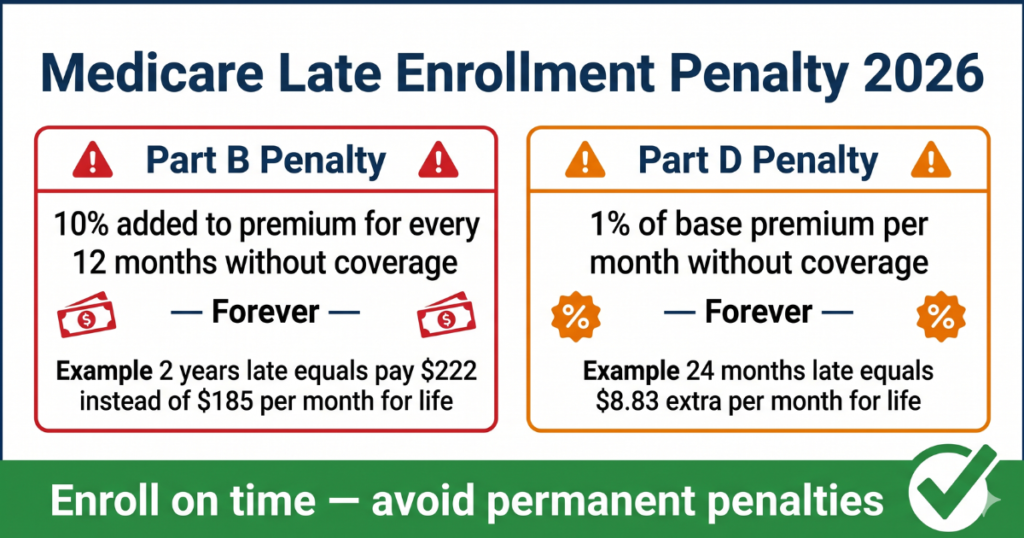

Medicare Part B late enrollment penalty — 10% added to your monthly Part B premium for every 12-month period you were eligible but did not enroll in Medicare Part B without qualifying coverage. This penalty is permanent and stays with you for life.

For example if you delay enrolling in Medicare Part B for 3 years without qualifying employer coverage you will pay 30% more than the standard Part B premium every month forever. At the 2026 standard premium of $185 per month that means paying $240.50 instead of $185 every single month for the rest of your life.

Medicare Part D late enrollment penalty — 1% of the national base beneficiary premium multiplied by the number of months you went without qualifying drug coverage. The 2026 national base beneficiary premium is $36.78. So for every month you delay enrolling in Medicare Part D without qualifying coverage you owe an additional $0.37 per month permanently.

If you delay Medicare Part D enrollment for 24 months your penalty is 24% of $36.78 = $8.83 per month added to your Part D premium forever.

These penalties are why knowing exactly when to enroll in Medicare is so critical. Always enroll on time.

When to Enroll in Medicare — A Complete Timeline by Age

Here is a complete timeline showing when to enroll in Medicare based on your age:

Age 63 — Start researching Medicare. Review your current health coverage. Understand the difference between Original Medicare and Medicare Advantage. Begin comparing Medigap supplement plans.

Age 64 and 9 months — Your Initial Enrollment Period opens. This is when to enroll in Medicare Part A and Part B for coverage starting on your 65th birthday. Enroll online at SSA.gov, by phone at 1-800-772-1213, or in person at your local Social Security office.

Age 65 — Medicare coverage begins if you enrolled during the first 3 months of your Initial Enrollment Period. If you are still working and have employer coverage you may continue delaying Part B enrollment without penalty.

Age 65 and 3 months — Your Initial Enrollment Period closes. If you have not enrolled in Medicare and do not have qualifying employer coverage you will face late enrollment penalties.

Every year October 15 to December 7 — Annual Open Enrollment Period. Review your Medicare coverage every year and make any needed changes. This is when to enroll in Medicare Advantage or Part D if you want to switch plans.

Frequently Asked Questions — When to Enroll in Medicare

When to enroll in Medicare for the first time?

The best time to enroll in Medicare for the first time is during the 3 months before the month you turn 65 — the first part of your Initial Enrollment Period. Enrolling during this window gives you the earliest possible coverage start date — the first day of your birthday month. If you miss this window you can still enroll during your birthday month or the 3 months after without penalty but your coverage start date will be delayed.

When to enroll in Medicare if I am still working at 65?

If you are still working at 65 and covered by employer group health insurance through a current employer with 20 or more employees you can delay Medicare Part B enrollment without penalty. You should still enroll in premium-free Medicare Part A at 65. When your employment or employer coverage ends you have an 8-month Special Enrollment Period to enroll in Medicare Part B without penalty.

When to enroll in Medicare Part D if I have no drug coverage?

If you have no other qualifying drug coverage you should enroll in Medicare Part D during your Initial Enrollment Period — the same 7-month window around your 65th birthday. Delaying Medicare Part D enrollment without qualifying coverage results in a permanent late enrollment penalty of 1% of the national base premium per month of delay.

When to enroll in Medicare if I am turning 65 and on COBRA?

COBRA coverage is not considered qualifying employer coverage for purposes of delaying Medicare enrollment. When you turn 65 and are on COBRA you should enroll in Medicare Part A and Part B during your Initial Enrollment Period. Delaying Medicare enrollment because of COBRA will result in late enrollment penalties.

When is the deadline to enroll in Medicare?

The deadline to enroll in Medicare without penalty for most people is the last day of their Initial Enrollment Period — 3 months after their 65th birthday month. For example if your birthday is July 15 your deadline to enroll in Medicare without penalty is October 31. After this deadline you must wait for the General Enrollment Period (January 1 to March 31) and will face permanent late enrollment penalties.

When to enroll in Medicare Advantage?

You can enroll in Medicare Advantage during your Initial Enrollment Period when you first become eligible for Medicare, during the Annual Open Enrollment Period (October 15 to December 7), during a Special Enrollment Period, or during the Medicare Advantage Open Enrollment Period (January 1 to March 31). You must be enrolled in both Medicare Part A and Part B before you can enroll in Medicare Advantage.

Can I enroll in Medicare before 65?

Yes. You can enroll in Medicare before 65 if you have received Social Security Disability Insurance (SSDI) for 24 months, have End-Stage Renal Disease (ESRD), or have ALS. If you have received SSDI for 24 months you are automatically enrolled in Medicare Parts A and B — you do not need to take any action to enroll in Medicare.

Summary — When to Enroll in Medicare 2026

Knowing exactly when to enroll in Medicare is critical to avoiding permanent late enrollment penalties that can cost you thousands of dollars over your lifetime. The answer to when to enroll in Medicare for most people is during the Initial Enrollment Period — the 7-month window starting 3 months before your 65th birthday.

If you are still working at 65 with employer coverage you can delay Medicare Part B enrollment without penalty but you must enroll within 8 months of your employment or employer coverage ending. Always enroll in premium-free Medicare Part A at 65 regardless of your working status.

Review your Medicare coverage every year during the Annual Open Enrollment Period from October 15 to December 7 to ensure you have the best coverage at the best price.

For free personalized help with Medicare enrollment contact your State Health Insurance Assistance Program (SHIP) counselor at shiphelp.org or call Medicare free at 1-800-633-4227.

This guide is for informational purposes only and is not medical or financial advice. Always verify current Medicare enrollment rules at Medicare.gov and SSA.gov.

Sources: Medicare.gov | SSA.gov | CMS.gov | AARP.org

Last updated: April 2026 | Author: James Carter, Independent Medicare Research Analyst