Medigap Plan G vs Plan N — Which is Better in 2026?

Medigap Plan G vs Plan N — which is better in 2026? This is the most common question seniors ask when shopping for Medicare supplement coverage. Both Medigap Plan G and Medigap Plan N are excellent Medicare supplement options in 2026 but they have key differences in coverage and cost that make one better than the other depending on your situation. In this complete comparison guide we break down exactly how Medigap Plan G vs Plan N compares in 2026 — coverage differences, cost differences, and which one is right for your specific healthcare needs. All information is sourced from Medicare.gov and CMS.gov.

Also Read-Does Medicare Cover Dental and Vision — Complete Guide 2026

What You Will Learn — Medigap Plan G vs Plan N

- The key difference between Medigap Plan G vs Plan N in 2026

- What Medigap Plan G covers in 2026

- What Medigap Plan N covers in 2026

- How much Medigap Plan G costs in 2026

- How much Medigap Plan N costs in 2026

- The complete side by side comparison of Medigap Plan G vs Plan N

- When Medigap Plan G is better than Plan N

- When Medigap Plan N is better than Plan G

- The math — which saves you more money

- Frequently asked questions about Medigap Plan G vs Plan N

Medigap Plan G vs Plan N — The Key Difference

The most important thing to understand about Medigap Plan G vs Plan N in 2026 is that both plans cover the Medicare Part A deductible of $1,676 per benefit period and both cover the Medicare Part B coinsurance of 20%. However Medigap Plan G vs Plan N differs in three specific areas:

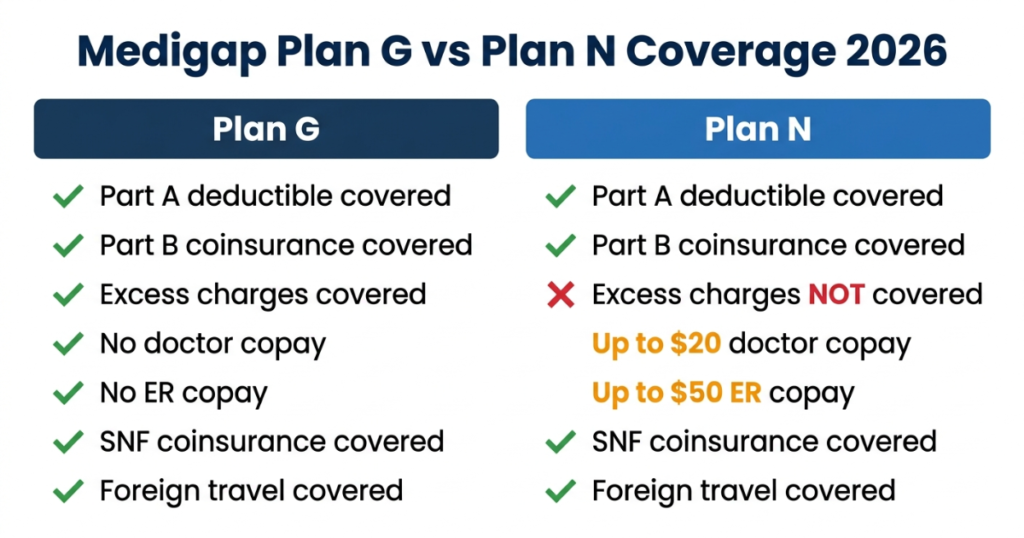

Medigap Plan G covers Part B excess charges — Plan N does not cover Part B excess charges.

Medigap Plan G has no doctor visit copays — Plan N charges up to $20 per doctor visit copay.

Medigap Plan G has no emergency room copays — Plan N charges up to $50 per emergency room visit that does not result in inpatient admission.

These three differences between Medigap Plan G vs Plan N are what determine which plan is better for you in 2026. If you visit doctors frequently or your doctors charge Part B excess charges Medigap Plan G may be the better choice. If you are relatively healthy and visit doctors infrequently Medigap Plan N may save you money through lower monthly premiums.

What Does Medigap Plan G Cover in 2026?

Medigap Plan G is the most comprehensive Medicare supplement plan available to new Medicare enrollees in 2026. Here is the complete list of what Medigap Plan G covers in 2026:

- Medicare Part A coinsurance and hospital costs up to 365 days after Medicare benefits are used — fully covered

- Medicare Part A deductible — $1,676 per benefit period — fully covered

- Medicare Part A hospice care coinsurance — fully covered

- Medicare Part B coinsurance — 20% of all approved outpatient services — fully covered after $257 deductible

- Medicare Part B excess charges — fully covered

- Skilled nursing facility coinsurance — $209.50 per day for days 21 to 100 — fully covered

- Foreign travel emergency coverage — up to plan limits after $250 deductible

- Blood — first 3 pints — fully covered

What Medigap Plan G does NOT cover in 2026:

- The Medicare Part B annual deductible of $257 — you pay this yourself once per year

- Routine dental, vision, or hearing care

- Prescription drugs — you need a separate Part D plan

With Medigap Plan G the only out-of-pocket cost you have after enrolling is the $257 annual Medicare Part B deductible. After paying that once per year Plan G covers 100% of all Medicare-approved costs for the rest of the year. This makes Medigap Plan G the most predictable and comprehensive coverage option among Medicare supplement plans in 2026.

What Does Medigap Plan N Cover in 2026?

Medigap Plan N covers almost everything Medigap Plan G covers in 2026 with three important exceptions. Here is the complete list of what Medigap Plan N covers in 2026:

- Medicare Part A coinsurance and hospital costs up to 365 days after Medicare benefits are used — fully covered

- Medicare Part A deductible — $1,676 per benefit period — fully covered

- Medicare Part A hospice care coinsurance — fully covered

- Medicare Part B coinsurance — 20% of all approved outpatient services — fully covered after $257 deductible

- Skilled nursing facility coinsurance — $209.50 per day for days 21 to 100 — fully covered

- Foreign travel emergency coverage — up to plan limits after $250 deductible

- Blood — first 3 pints — fully covered

What Medigap Plan N does NOT cover in 2026:

- The Medicare Part B annual deductible of $257 — you pay this yourself

- Part B excess charges — you pay these yourself

- Doctor visit copays — up to $20 per visit

- Emergency room copays — up to $50 per visit that does not result in admission

- Routine dental, vision, or hearing care

- Prescription drugs — you need a separate Part D plan

Medigap Plan G vs Plan N — Complete Coverage Comparison 2026

Here is the complete side by side coverage comparison of Medigap Plan G vs Plan N in 2026:

Medicare Part A deductible ($1,676 per benefit period) Plan G — Covered 100% Plan N — Covered 100% Winner — Tie ✅

Medicare Part A coinsurance Plan G — Covered 100% Plan N — Covered 100% Winner — Tie ✅

Medicare Part B deductible ($257 per year) Plan G — NOT covered — you pay $257 per year Plan N — NOT covered — you pay $257 per year Winner — Tie ✅

Medicare Part B coinsurance (20%) Plan G — Covered 100% after $257 deductible Plan N — Covered 100% after $257 deductible Winner — Tie ✅

Medicare Part B excess charges Plan G — Covered 100% Plan N — NOT covered — you pay excess charges Winner — Plan G ✅

Doctor visit copay Plan G — $0 copay Plan N — Up to $20 copay per visit Winner — Plan G ✅

Emergency room copay Plan G — $0 copay Plan N — Up to $50 copay per ER visit not resulting in admission Winner — Plan G ✅

Skilled nursing facility coinsurance Plan G — Covered 100% Plan N — Covered 100% Winner — Tie ✅

Foreign travel emergency Plan G — Covered up to plan limits after $250 deductible Plan N — Covered up to plan limits after $250 deductible Winner — Tie ✅

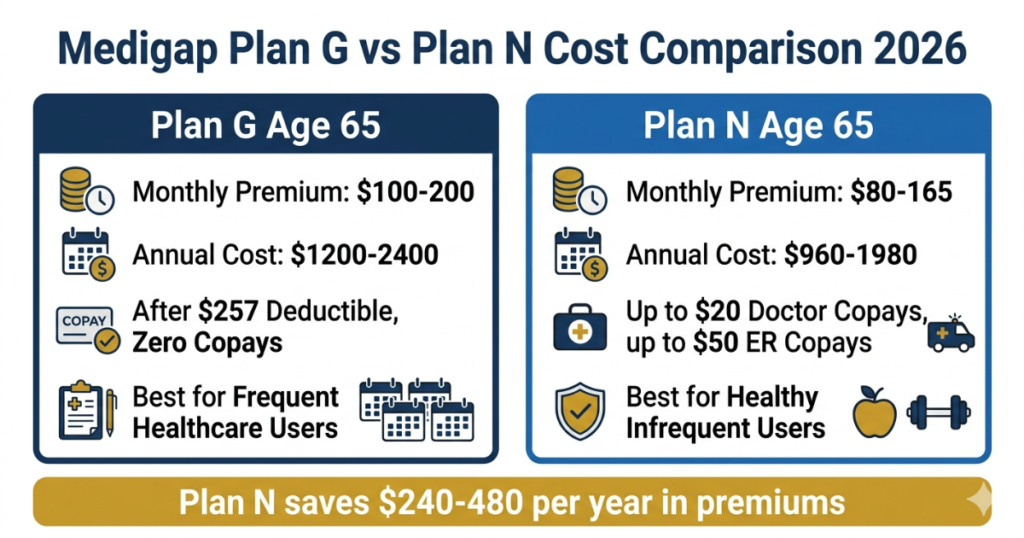

How Much Does Medigap Plan G Cost in 2026?

Medigap Plan G premiums in 2026 vary based on your age, gender, location, tobacco use, and the insurance company you choose. Since Medigap benefits are standardized the only variable between companies is the monthly premium — making it important to compare prices from multiple insurers.

Average Medigap Plan G monthly premiums in 2026 by age:

- Age 65 female non-smoker — $100 to $180 per month

- Age 65 male non-smoker — $110 to $200 per month

- Age 70 female non-smoker — $130 to $220 per month

- Age 70 male non-smoker — $145 to $245 per month

- Age 75 female non-smoker — $160 to $270 per month

- Age 75 male non-smoker — $180 to $300 per month

Total annual cost of Medigap Plan G at age 65 in 2026 (including Part B premium, Part D, and Plan G):

- Part B premium — $185.00 per month = $2,220 per year

- Medigap Plan G — $150 per month average = $1,800 per year

- Part D drug plan — $46.50 per month average = $558 per year

- Part B annual deductible — $257 per year

- Total estimated annual cost — approximately $4,835 per year

With Medigap Plan G your total annual Medicare costs are highly predictable because after the $257 deductible Plan G covers virtually everything else.

How Much Does Medigap Plan N Cost in 2026?

Medigap Plan N premiums in 2026 are typically 15% to 25% lower than Medigap Plan G premiums. This premium savings is the main reason many seniors choose Plan N over Plan G in 2026.

Average Medigap Plan N monthly premiums in 2026 by age:

- Age 65 female non-smoker — $80 to $150 per month

- Age 65 male non-smoker — $90 to $165 per month

- Age 70 female non-smoker — $105 to $185 per month

- Age 70 male non-smoker — $115 to $205 per month

- Age 75 female non-smoker — $130 to $220 per month

- Age 75 male non-smoker — $145 to $240 per month

Total annual cost of Medigap Plan N at age 65 in 2026 (including Part B premium, Part D, and Plan N):

- Part B premium — $185.00 per month = $2,220 per year

- Medigap Plan N — $120 per month average = $1,440 per year

- Part D drug plan — $46.50 per month average = $558 per year

- Part B annual deductible — $257 per year

- Estimated doctor visit copays (6 visits at $20) — $120 per year

- Total estimated annual cost — approximately $4,595 per year

For a healthy senior with infrequent doctor visits Medigap Plan N can save approximately $240 or more per year compared to Medigap Plan G.

Medigap Plan G vs Plan N — The Math in 2026

The decision between Medigap Plan G vs Plan N ultimately comes down to numbers. Here is the complete financial analysis for Medigap Plan G vs Plan N in 2026:

Assumption — Plan G costs $150/month and Plan N costs $120/month

Monthly premium difference — $30 per month Annual premium difference — $360 per year

This means Plan G costs $360 more per year in premiums than Plan N. For Plan G to be the better financial value you would need to pay more than $360 per year in Plan N copays and excess charges.

How many doctor visits make Plan G worth it?

If each doctor visit costs $20 under Plan N you would need 18 doctor visits per year for the Plan N copays to equal the $360 premium difference. Most seniors average 7 to 8 doctor visits per year — meaning Plan N would save most healthy seniors money.

However if your doctors charge Part B excess charges the calculation changes significantly. Part B excess charges can be up to 15% above the Medicare-approved amount. For a senior who regularly sees doctors that charge excess charges Plan G quickly becomes the better financial value.

The real-world Medigap Plan G vs Plan N calculation:

Scenario A — Healthy senior with 6 doctor visits per year and no excess charges:

- Plan N copays — 6 visits x $20 = $120 per year

- Plan G premium extra cost — $360 per year

- Plan N saves — $240 per year

- Winner — Plan N

Scenario B — Senior with 20 doctor visits per year and no excess charges:

- Plan N copays — 20 visits x $20 = $400 per year

- Plan G premium extra cost — $360 per year

- Plan G saves — $40 per year

- Winner — Plan G (barely)

Scenario C — Senior with doctors charging excess charges:

- Potential excess charges — $500 to $2,000+ per year

- Plan G premium extra cost — $360 per year

- Plan G saves — $140 to $1,640 per year

- Winner — Plan G by a large margin

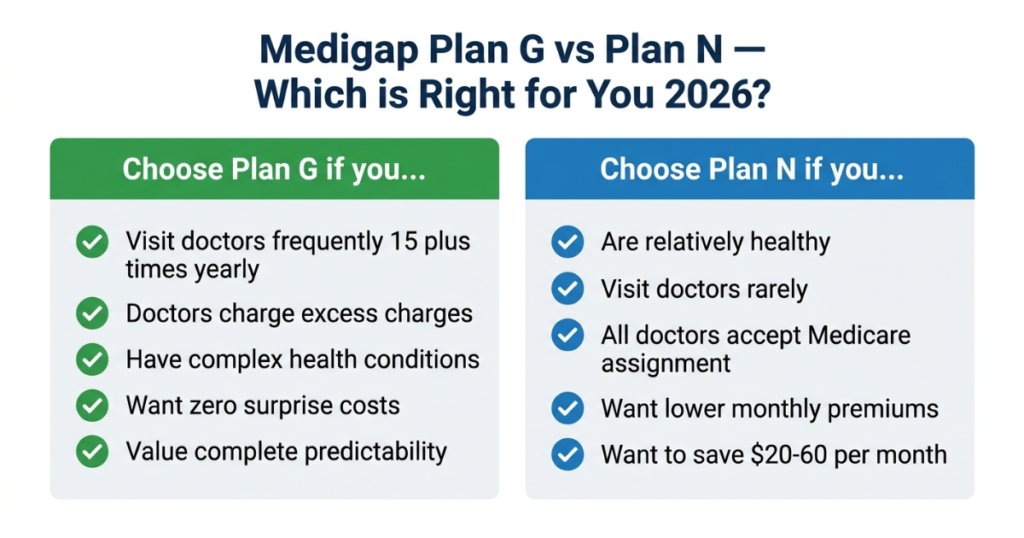

When is Medigap Plan G Better Than Plan N?

Medigap Plan G is better than Plan N in 2026 in these situations:

You visit doctors frequently — if you have 15 or more doctor visits per year the $20 copays under Plan N add up to $300 or more annually — approaching the premium difference between the plans.

Your doctors charge Part B excess charges — if any of your doctors do not accept Medicare assignment they can charge up to 15% above the Medicare-approved amount. Plan G covers these excess charges completely while Plan N leaves you responsible for them.

You have complex health conditions — seniors with ongoing chronic conditions, multiple specialists, and frequent medical needs benefit most from the comprehensive zero-copay coverage of Medigap Plan G.

You want completely predictable costs — Medigap Plan G gives you the most predictable annual Medicare costs. After paying the $257 Part B deductible you know exactly what your costs will be for the rest of the year — essentially zero for covered services.

You value simplicity — Medigap Plan G requires no tracking of copays or worrying about excess charges. Every covered Medicare service is paid in full after your annual deductible.

When is Medigap Plan N Better Than Plan G?

Medigap Plan N is better than Plan G in 2026 in these situations:

You are relatively healthy — if you visit doctors infrequently the $20 copays under Plan N will be minimal and the premium savings of $20 to $60 per month will easily outweigh your copay costs.

Your doctors accept Medicare assignment — if all your doctors accept Medicare assignment they cannot charge Part B excess charges. In this case there is no financial risk from Plan N’s lack of excess charge coverage.

You want to reduce monthly premiums — if cash flow is a concern the lower monthly premium of Medigap Plan N provides immediate savings every month.

You are enrolling at a younger age — younger Medicare enrollees often start with Medigap Plan N to take advantage of lower premiums during their healthier years and can always switch to Plan G later (subject to underwriting in most states).

Medigap Plan G vs Plan N — What Are Part B Excess Charges?

Part B excess charges are one of the most misunderstood aspects of the Medigap Plan G vs Plan N comparison. Here is what you need to know:

Medicare-participating doctors accept the Medicare-approved amount as payment in full. These doctors cannot charge excess charges — so Plan N’s lack of excess charge coverage does not matter for visits to these doctors.

Medicare non-participating doctors can charge up to 15% more than the Medicare-approved amount. This additional 15% is called a Part B excess charge. Medigap Plan G covers these excess charges completely. Medigap Plan N does NOT cover excess charges — you pay them out of pocket.

The key question for the Medigap Plan G vs Plan N decision is whether any of your current or future doctors charge Part B excess charges. You can check whether your doctor accepts Medicare assignment by calling their office or checking Medicare’s physician finder tool at Medicare.gov.

In most areas of the United States the majority of doctors accept Medicare assignment and do not charge excess charges. However in certain high-cost urban areas and with certain specialist types excess charges are more common. If you live in an area with high proportions of non-participating Medicare providers Medigap Plan G is clearly the safer choice.

Frequently Asked Questions — Medigap Plan G vs Plan N

What is the main difference between Medigap Plan G and Plan N in 2026?

The main differences between Medigap Plan G vs Plan N in 2026 are three things Plan G covers that Plan N does not — Part B excess charges, doctor visit copays of up to $20, and emergency room copays of up to $50. Plan N has lower monthly premiums than Plan G typically by $20 to $60 per month. Both plans cover the Part A deductible, Part B coinsurance, skilled nursing facility coinsurance, and foreign travel emergency coverage.

Is Medigap Plan G worth the extra cost over Plan N in 2026?

Whether Medigap Plan G is worth the extra cost over Plan N depends on your healthcare usage. If you visit doctors frequently — 15 or more times per year — or if your doctors charge Part B excess charges Plan G is likely worth the higher premium. If you are relatively healthy with infrequent doctor visits and all your doctors accept Medicare assignment Plan N will likely save you money through lower premiums.

How much cheaper is Medigap Plan N than Plan G in 2026?

Medigap Plan N is typically 15% to 25% cheaper than Plan G in 2026. For a 65-year-old non-smoking female the monthly premium difference is approximately $20 to $40 per month — or $240 to $480 per year. The exact difference varies by location, age, and insurance company.

Can I switch from Medigap Plan N to Plan G later?

You can apply to switch from Medigap Plan N to Plan G at any time. However outside of your Medigap Open Enrollment Period most states allow insurance companies to use medical underwriting — meaning they can charge you more or deny coverage based on your health status. If you are in good health when you first enroll consider whether your long-term health needs might favor starting with Plan G.

Does Medigap Plan N cover emergency room visits?

Medigap Plan N covers emergency room visits but with a copay of up to $50 per visit that does not result in an inpatient hospital admission. If your ER visit results in inpatient admission the copay is waived. Medigap Plan G covers emergency room visits with no copay at all.

Do both Medigap Plan G and Plan N cover foreign travel emergencies?

Yes. Both Medigap Plan G and Plan N include foreign travel emergency coverage. Both plans cover 80% of medically necessary emergency care outside the United States after a $250 deductible up to a $50,000 lifetime limit. This benefit is particularly valuable for seniors who travel internationally.

Which Medigap plan is most popular in 2026 — Plan G or Plan N?

Medigap Plan G is the most popular Medicare supplement plan in 2026 — more seniors choose Plan G than any other Medigap plan. However Medigap Plan N is the fastest growing Medigap plan as more seniors recognize the value of its lower premiums. Both Plan G and Plan N are excellent choices and the best option depends entirely on your personal healthcare situation.

Summary — Medigap Plan G vs Plan N 2026

Medigap Plan G vs Plan N is ultimately a decision between comprehensive coverage and lower premiums. Medigap Plan G offers the most complete coverage available to new Medicare enrollees in 2026 — after the $257 annual deductible Plan G covers 100% of all Medicare-approved costs with no copays and no excess charge exposure. Medigap Plan N offers very similar coverage at a lower monthly premium but with up to $20 doctor visit copays, up to $50 ER copays, and no excess charge coverage.

The best choice between Medigap Plan G vs Plan N in 2026 depends on how often you use healthcare services, whether your doctors charge Part B excess charges, and how much you value cost predictability versus premium savings. Most seniors with frequent medical needs or complex health conditions choose Plan G. Most relatively healthy seniors who visit doctors infrequently choose Plan N for the premium savings.

To compare specific Medigap Plan G vs Plan N premiums in your area contact multiple insurance companies for quotes or use a licensed Medicare insurance agent. For free unbiased help comparing Medigap Plan G vs Plan N contact your State Health Insurance Assistance Program (SHIP) counselor at shiphelp.org or call Medicare free at 1-800-633-4227.

This guide is for informational purposes only and is not financial or medical advice. Always verify current Medigap plan details and costs with licensed insurance agents in your state before making enrollment decisions.

Sources: Medicare.gov | CMS.gov | SSA.gov | AARP.org

Last updated: April 2026 | Author: James Carter, Independent Medicare Research Analyst

One Comment