Medicare Late Enrollment Penalty — How to Avoid It in 2026

The Medicare late enrollment penalty is one of the most costly mistakes a senior can make when signing up for Medicare. The Medicare late enrollment penalty is permanent — it stays with you every single month for the rest of your life. In this complete 2026 guide we explain exactly what the Medicare late enrollment penalty is, how the Medicare late enrollment penalty is calculated, how to avoid the Medicare late enrollment penalty, and what to do if you have already been charged a Medicare late enrollment penalty. All information is sourced from Medicare.gov and SSA.gov.

Also Read- Medicare Part A vs Part B — What Is the Difference in 2026? Also Read- Best Medicare Plans in Ohio 2026 — Complete Guide

What You Will Learn — Medicare Late Enrollment Penalty

- What the Medicare late enrollment penalty is

- The Medicare Part B late enrollment penalty explained

- The Medicare Part D late enrollment penalty explained

- How the Medicare late enrollment penalty is calculated

- How much the Medicare late enrollment penalty costs in 2026

- How to avoid the Medicare late enrollment penalty

- How to appeal the Medicare late enrollment penalty

- Situations where the Medicare late enrollment penalty does not apply

- Frequently asked questions about the Medicare late enrollment penalty

What Is the Medicare Late Enrollment Penalty?

The Medicare late enrollment penalty is a permanent surcharge added to your Medicare premiums when you delay enrolling in Medicare without having other qualifying health coverage. The Medicare late enrollment penalty was designed to encourage seniors to enroll in Medicare when they first become eligible rather than waiting until they need medical care.

The Medicare late enrollment penalty applies to Medicare Part B and Medicare Part D. There is no late enrollment penalty for Medicare Part A for most people because Part A is free for seniors who worked 10 or more years and paid Medicare taxes.

The most important thing to understand about the Medicare late enrollment penalty is that it is permanent. Unlike a temporary fee the Medicare late enrollment penalty is added to your premium every single month for as long as you have Medicare. A senior who faces a Medicare late enrollment penalty at age 65 will still be paying that penalty at age 75, 80, and beyond.

Medicare Part B Late Enrollment Penalty — Explained

The Medicare Part B late enrollment penalty is the most significant and most costly of the Medicare late enrollment penalties. Here is everything you need to know about the Medicare Part B late enrollment penalty:

What triggers the Medicare Part B late enrollment penalty?

The Medicare Part B late enrollment penalty is triggered when you delay enrolling in Medicare Part B past your Initial Enrollment Period without having qualifying employer group health coverage from a current employer. The Medicare Part B late enrollment penalty begins accruing from the end of your Initial Enrollment Period.

How is the Medicare Part B late enrollment penalty calculated?

The Medicare Part B late enrollment penalty is 10% of the standard Part B premium for every full 12-month period you were eligible for Medicare Part B but did not enroll without qualifying coverage.

The formula for the Medicare Part B late enrollment penalty is:

Number of full 12-month periods without coverage multiplied by 10% multiplied by the current standard Part B premium equals your monthly Medicare Part B late enrollment penalty.

Medicare Part B Late Enrollment Penalty Examples in 2026:

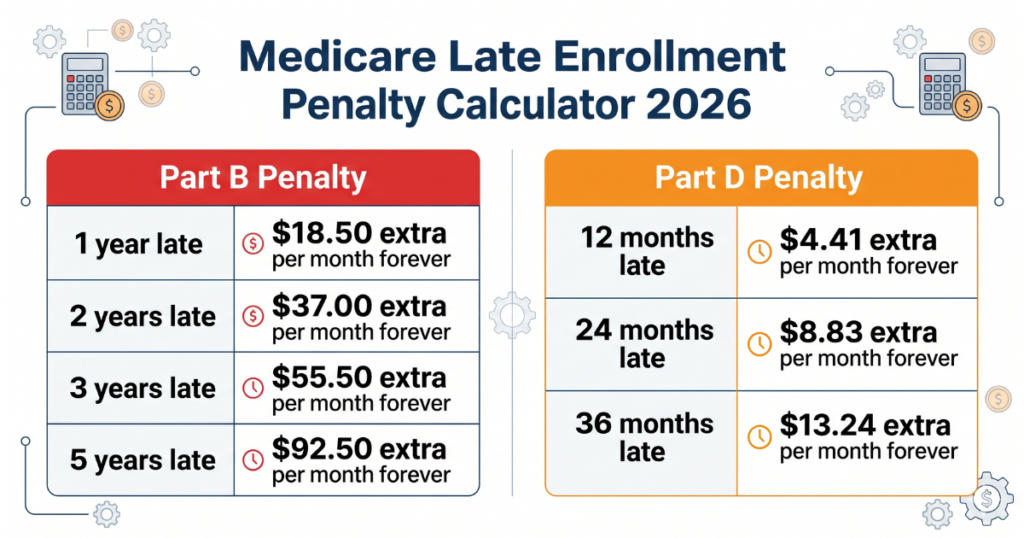

The standard Medicare Part B premium in 2026 is $185.00 per month.

If you delayed Medicare Part B enrollment for 1 year — your Medicare Part B late enrollment penalty is 10% of $185.00 = $18.50 per month added to your premium forever. You pay $203.50 per month instead of $185.00.

If you delayed Medicare Part B enrollment for 2 years — your Medicare Part B late enrollment penalty is 20% of $185.00 = $37.00 per month added forever. You pay $222.00 per month instead of $185.00.

If you delayed Medicare Part B enrollment for 3 years — your Medicare Part B late enrollment penalty is 30% of $185.00 = $55.50 per month added forever. You pay $240.50 per month instead of $185.00.

If you delayed Medicare Part B enrollment for 5 years — your Medicare Part B late enrollment penalty is 50% of $185.00 = $92.50 per month added forever. You pay $277.50 per month instead of $185.00.

The Medicare Part B late enrollment penalty grows as premiums increase. Because the penalty is calculated as a percentage of the current premium every time Medicare Part B premiums increase your Medicare Part B late enrollment penalty also increases. This means the Medicare Part B late enrollment penalty becomes more expensive over time — not just a fixed dollar amount.

Medicare Part D Late Enrollment Penalty — Explained

The Medicare Part D late enrollment penalty applies when you delay enrolling in Medicare prescription drug coverage without having other qualifying drug coverage. Here is everything you need to know about the Medicare Part D late enrollment penalty:

What triggers the Medicare Part D late enrollment penalty?

The Medicare Part D late enrollment penalty is triggered when you go 63 or more consecutive days without Medicare Part D drug coverage or other qualifying prescription drug coverage after your Initial Enrollment Period ends.

How is the Medicare Part D late enrollment penalty calculated?

The Medicare Part D late enrollment penalty is 1% of the national base beneficiary premium for every month you went without qualifying drug coverage. The Medicare Part D late enrollment penalty is rounded to the nearest $0.10.

The national base beneficiary premium for Medicare Part D in 2026 is $36.78.

The formula for the Medicare Part D late enrollment penalty is:

Number of months without qualifying drug coverage multiplied by 1% multiplied by $36.78 equals your monthly Medicare Part D late enrollment penalty.

Medicare Part D Late Enrollment Penalty Examples in 2026:

If you went 12 months without qualifying drug coverage — your Medicare Part D late enrollment penalty is 12% of $36.78 = $4.41 per month added to your Part D premium forever.

If you went 24 months without qualifying drug coverage — your Medicare Part D late enrollment penalty is 24% of $36.78 = $8.83 per month added forever.

If you went 36 months without qualifying drug coverage — your Medicare Part D late enrollment penalty is 36% of $36.78 = $13.24 per month added forever.

If you went 60 months without qualifying drug coverage — your Medicare Part D late enrollment penalty is 60% of $36.78 = $22.07 per month added forever.

The Medicare Part D late enrollment penalty is recalculated every year because it is based on the current national base beneficiary premium which changes annually. This means your Medicare Part D late enrollment penalty may change slightly each year as the national base premium fluctuates.

How Much Does the Medicare Late Enrollment Penalty Cost Over a Lifetime?

The true cost of the Medicare late enrollment penalty becomes clear when you calculate the lifetime impact. Here is how much the Medicare late enrollment penalty costs over a lifetime in 2026:

Medicare Part B late enrollment penalty lifetime cost:

If you delayed Part B enrollment by 2 years your monthly Medicare Part B late enrollment penalty is $37.00 per month.

Over 10 years that is $4,440 in extra premiums due to the Medicare Part B late enrollment penalty. Over 20 years that is $8,880 in extra premiums due to the Medicare Part B late enrollment penalty.

And remember — the Medicare Part B late enrollment penalty increases every year as the standard premium increases.

Medicare Part D late enrollment penalty lifetime cost:

If you delayed Part D enrollment by 24 months your monthly Medicare Part D late enrollment penalty is $8.83 per month.

Over 10 years that is $1,059.60 in extra premiums due to the Medicare Part D late enrollment penalty. Over 20 years that is $2,119.20 in extra premiums due to the Medicare Part D late enrollment penalty.

Combined Medicare late enrollment penalty cost for 2 years of delayed enrollment in both Part B and Part D — over $10,000 in extra lifetime premiums. This is why avoiding the Medicare late enrollment penalty is so critically important.

How to Avoid the Medicare Late Enrollment Penalty

Avoiding the Medicare late enrollment penalty is simple if you follow these rules:

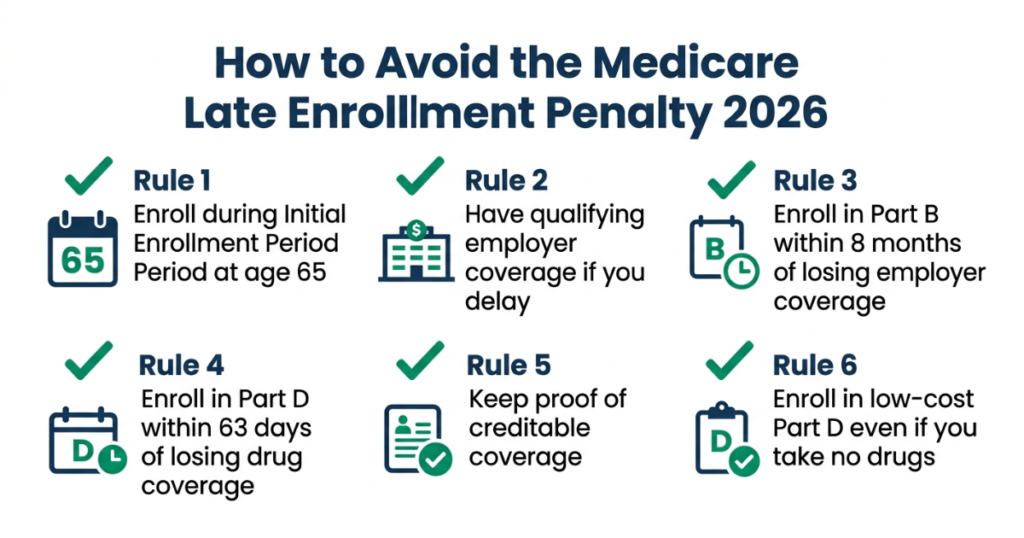

Rule 1 — Enroll in Medicare during your Initial Enrollment Period

The most reliable way to avoid the Medicare late enrollment penalty is to enroll in Medicare Parts A, B, and D during your Initial Enrollment Period — the 7-month window starting 3 months before your 65th birthday. Enrolling during your Initial Enrollment Period guarantees you will never face the Medicare late enrollment penalty.

Rule 2 — Have qualifying employer coverage if you delay

The only valid reason to delay Medicare enrollment without facing the Medicare late enrollment penalty is if you have qualifying employer group health coverage from a current employer. Coverage must be from your own or your spouse’s active employment — not COBRA, retiree health coverage, or VA benefits.

Rule 3 — Enroll within 8 months of losing employer coverage

If you have been delaying Medicare enrollment because of employer coverage you must enroll in Medicare Part B within 8 months of your employment or employer coverage ending to avoid the Medicare Part B late enrollment penalty. Do not wait even one day past this 8-month Special Enrollment Period.

Rule 4 — Enroll in Part D within 63 days of losing drug coverage

If you had qualifying drug coverage from an employer or other source you must enroll in Medicare Part D within 63 days of losing that coverage to avoid the Medicare Part D late enrollment penalty. The 63-day clock starts the day after your other drug coverage ends.

Rule 5 — Get a notice of creditable coverage

If you have employer drug coverage ask your employer for a notice of creditable coverage. This document confirms your coverage qualifies as at least as good as Medicare Part D. Keep this document — you will need it as proof when you eventually enroll in Medicare Part D to demonstrate you should not face the Medicare Part D late enrollment penalty.

Rule 6 — Enroll in a low-cost Part D plan even if you take no drugs

If you take no prescription medications a simple low-cost Medicare Part D plan — some cost as little as $5 to $15 per month — protects you from the Medicare Part D late enrollment penalty forever. The cost of a basic plan is far less than the cumulative Medicare Part D late enrollment penalty you would face after even one year of delayed enrollment.

Situations Where the Medicare Late Enrollment Penalty Does NOT Apply

There are specific situations where you are exempt from the Medicare late enrollment penalty. The Medicare late enrollment penalty does not apply in these cases:

Active employer coverage exemption

You are exempt from the Medicare Part B late enrollment penalty if you delayed enrollment because you were covered by employer group health insurance through your own or your spouse’s active current employment. The employer must have 20 or more employees for this exemption to apply to Part B.

Creditable drug coverage exemption

You are exempt from the Medicare Part D late enrollment penalty if you had other creditable prescription drug coverage — such as employer drug coverage, VA drug benefits, or TRICARE — for the entire time you were eligible for Medicare Part D. You must be able to prove continuous creditable coverage to avoid the Medicare Part D late enrollment penalty.

Extra Help exemption

If you qualify for Extra Help — the Low Income Subsidy program for Medicare Part D — you are automatically exempt from the Medicare Part D late enrollment penalty regardless of when you enroll.

Incarceration exemption

If you were incarcerated during the period you missed Medicare enrollment you may be exempt from the Medicare late enrollment penalty for that period. Documentation of incarceration dates is required.

ICEP exemption for Medicare Advantage

There is no late enrollment penalty for Medicare Advantage plans. The Medicare late enrollment penalty for Part B still applies but there is no separate Advantage late enrollment penalty.

How to Appeal the Medicare Late Enrollment Penalty

If you believe your Medicare late enrollment penalty was assessed in error you have the right to appeal. Here is how to appeal the Medicare late enrollment penalty:

Step 1 — Request a review

Contact Social Security Administration at 1-800-772-1213 or visit your local Social Security office. Explain that you believe the Medicare late enrollment penalty was assessed in error and request a reconsideration.

Step 2 — Gather your documentation

Collect all documentation proving you had qualifying coverage during the period Medicare says you did not. This includes employer insurance cards, Explanation of Benefits statements, letters from your employer’s HR department confirming your coverage dates, and notices of creditable coverage for Part D.

Step 3 — Submit your appeal in writing

Write a formal appeal letter explaining why you believe the Medicare late enrollment penalty should not apply to your situation. Attach all supporting documentation. Send by certified mail so you have proof of delivery.

Step 4 — Wait for a decision

Medicare will review your appeal and issue a written decision. If your appeal is approved the Medicare late enrollment penalty will be removed from your premiums. If your appeal is denied you can request a second level of appeal.

Step 5 — Escalate if needed

If your initial appeal is denied you can request a hearing before an Administrative Law Judge if the amount in dispute meets the minimum threshold. Contact a Medicare counselor at shiphelp.org for free help with your Medicare late enrollment penalty appeal.

Medicare Late Enrollment Penalty — Common Mistakes to Avoid

These are the most common mistakes that lead to the Medicare late enrollment penalty:

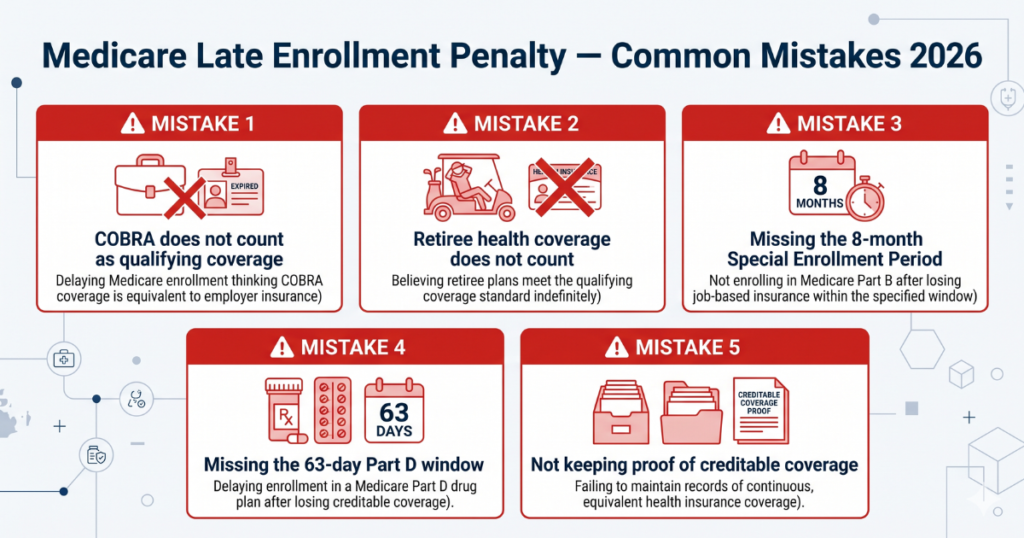

Mistake 1 — Assuming COBRA counts as qualifying coverage. COBRA does not protect you from the Medicare late enrollment penalty. When you turn 65 on COBRA you must enroll in Medicare Parts A and B during your Initial Enrollment Period.

Mistake 2 — Assuming retiree health coverage counts as qualifying coverage. Retiree health coverage from a former employer does not protect you from the Medicare late enrollment penalty. Only active employer coverage from current employment counts.

Mistake 3 — Missing the 8-month Special Enrollment Period. After your employer coverage ends you have exactly 8 months to enroll in Medicare Part B without facing the Medicare late enrollment penalty. Missing this window even by one day means waiting for the General Enrollment Period and paying the penalty.

Mistake 4 — Missing the 63-day Part D window. After your qualifying drug coverage ends you have exactly 63 days to enroll in Medicare Part D without facing the Medicare Part D late enrollment penalty. Mark this date on your calendar immediately when your other coverage ends.

Mistake 5 — Not keeping proof of creditable coverage. If you had employer drug coverage and later enroll in Medicare Part D without documentation of your continuous coverage you may be incorrectly charged the Medicare Part D late enrollment penalty. Always keep your notices of creditable coverage.

Frequently Asked Questions — Medicare Late Enrollment Penalty

What is the Medicare late enrollment penalty?

The Medicare late enrollment penalty is a permanent surcharge added to your Medicare Part B and Part D premiums when you delay enrolling in Medicare without having qualifying coverage. The Medicare Part B late enrollment penalty is 10% of the standard Part B premium for every 12 months you delayed enrollment. The Medicare Part D late enrollment penalty is 1% of the national base premium for every month you delayed enrollment. Both penalties are permanent and stay with you for life.

How do I calculate my Medicare late enrollment penalty?

To calculate your Medicare Part B late enrollment penalty multiply the number of full 12-month periods you went without Medicare Part B coverage by 10% then multiply by the current standard Part B premium of $185.00 in 2026. To calculate your Medicare Part D late enrollment penalty multiply the number of months without qualifying drug coverage by 1% then multiply by the 2026 national base premium of $36.78.

Can the Medicare late enrollment penalty be waived?

The Medicare late enrollment penalty can be waived if you successfully appeal it by proving you had qualifying coverage during the period of delayed enrollment. The Social Security Administration reviews Medicare late enrollment penalty appeals. You must provide documentation of your qualifying coverage to have the Medicare late enrollment penalty waived.

Does the Medicare late enrollment penalty ever go away?

No. The Medicare late enrollment penalty is permanent. Once assessed the Medicare late enrollment penalty stays on your account for as long as you have Medicare. The only way to remove the Medicare late enrollment penalty is to successfully appeal it by proving you had qualifying coverage during the delayed enrollment period.

Is there a Medicare late enrollment penalty for Part A?

Most people do not face a Medicare late enrollment penalty for Part A because Part A is free for seniors who worked 10 or more years. If you must pay a premium for Part A and you delay enrollment there is a Medicare Part A late enrollment penalty of 10% of the Part A premium added for twice the number of years you delayed enrollment.

Does COBRA coverage protect me from the Medicare late enrollment penalty?

No. COBRA coverage does not protect you from the Medicare late enrollment penalty. When you turn 65 and are on COBRA you must enroll in Medicare Parts A and B during your Initial Enrollment Period. Delaying Medicare enrollment because of COBRA coverage will result in the Medicare late enrollment penalty.

What if I did not know about the Medicare late enrollment penalty?

Unfortunately not knowing about the Medicare late enrollment penalty is not a valid reason for having it waived. The Medicare late enrollment penalty applies regardless of whether you knew about it. This is why understanding the Medicare late enrollment penalty before you turn 65 is so important.

Summary — Medicare Late Enrollment Penalty 2026

The Medicare late enrollment penalty is one of the most financially damaging mistakes a senior can make. The Medicare Part B late enrollment penalty of 10% per year of delay and the Medicare Part D late enrollment penalty of 1% per month of delay are both permanent — they stay with you for life and cost thousands of extra dollars in premiums over your retirement.

Avoiding the Medicare late enrollment penalty is straightforward — enroll in Medicare during your Initial Enrollment Period unless you have qualifying employer coverage from a current employer. If you have employer coverage enroll in Medicare Part B within 8 months and Medicare Part D within 63 days of losing that coverage.

If you believe you have been incorrectly charged the Medicare late enrollment penalty contact your free SHIP counselor at shiphelp.org for help appealing the penalty or call Medicare at 1-800-633-4227.

This guide is for informational purposes only and is not medical or financial advice. Always verify current Medicare late enrollment penalty rules at Medicare.gov and SSA.gov.

Sources: Medicare.gov | SSA.gov | CMS.gov | AARP.org

Last updated: April 2026 | Author: James Carter, Independent Medicare Research Analyst

Also Read- Best Medicare Plans in Michigan 2026 — Top Rated Advantage Plans by County

2 Comments