Medicare Income Limits and IRMAA Surcharges 2026 — Complete Guide

Medicare income limits in 2026 determine how much you pay for your Medicare Part B and Part D premiums. If your income exceeds the Medicare income limits in 2026 you will pay more than the standard Medicare premium through surcharges called IRMAA — Income Related Monthly Adjustment Amount. Understanding the Medicare income limits in 2026 is critical for accurate retirement planning because many seniors are surprised to discover they owe significantly more than the standard Medicare premium. In this complete guide we explain exactly what the Medicare income limits are in 2026, the complete IRMAA surcharge tables, how the Medicare income limits in 2026 are calculated, and how to reduce your Medicare costs if you exceed the income limits. All information is sourced from Medicare.gov and CMS.gov.

Also Read-Does Medicare Cover Dental and Vision — Complete Guide 2026 Also Read- Best Medicare Plans in Pennsylvania 2026 — Complete Guide

What You Will Learn — Medicare Income Limits 2026

- What the Medicare income limits are in 2026

- The complete Medicare IRMAA income brackets for 2026

- How the Medicare income limits in 2026 are determined

- Which income counts toward the Medicare income limits 2026

- How IRMAA affects your Medicare Part B premium in 2026

- How IRMAA affects your Medicare Part D premium in 2026

- How to appeal the Medicare income limits surcharge in 2026

- How to reduce your Medicare costs if you exceed income limits

- Frequently asked questions about Medicare income limits 2026

What Are the Medicare Income Limits in 2026?

The Medicare income limits in 2026 are the income thresholds that determine whether you pay the standard Medicare premium or a higher income-adjusted premium through IRMAA surcharges. Most Medicare beneficiaries pay the standard Medicare Part B premium of $185.00 per month in 2026 because their income falls below the Medicare income limits.

The Medicare income limits in 2026 are based on your Modified Adjusted Gross Income (MAGI) reported on your federal income tax return from two years prior. This means the Medicare income limits in 2026 are based on your 2024 income tax return. Medicare uses a two-year lookback period because your most recent tax return may not yet be filed when Medicare sets your premium.

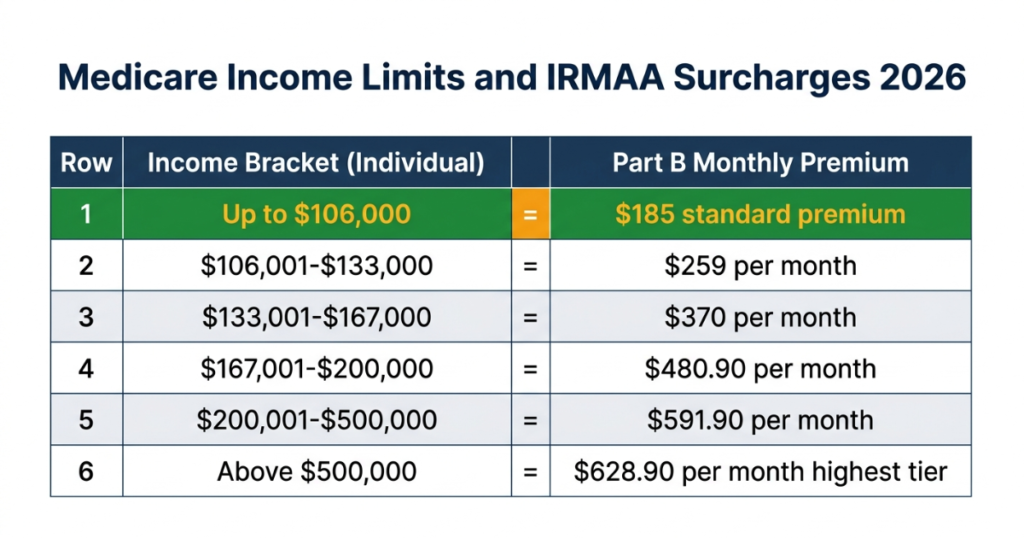

The standard Medicare income limit in 2026 is $106,000 for individuals and $212,000 for married couples filing jointly. If your 2024 income was at or below these Medicare income limits you pay the standard Part B premium of $185.00 per month in 2026. If your 2024 income exceeded these Medicare income limits you pay additional IRMAA surcharges on top of the standard premium.

Understanding the Medicare income limits in 2026 is especially important for recent retirees who had higher working income in previous years, seniors who took large IRA distributions or had significant investment income in 2024, and couples whose combined income approaches or exceeds the Medicare income limits in 2026.

Complete Medicare Income Limits and IRMAA Table 2026

Here is the complete Medicare income limits and IRMAA surcharge table for 2026. The Medicare income limits in 2026 create five tiers of premiums above the standard rate:

Tier 1 — Standard Medicare Income Limit 2026 Individual income up to $106,000 or joint income up to $212,000:

- Medicare Part B premium — $185.00 per month

- Medicare Part D IRMAA — $0 additional

Tier 2 — First Medicare Income Limit Threshold 2026 Individual income $106,001 to $133,000 or joint $212,001 to $266,000:

- Medicare Part B premium — $259.00 per month

- Medicare Part D IRMAA — $13.70 additional per month

Tier 3 — Second Medicare Income Limit Threshold 2026 Individual income $133,001 to $167,000 or joint $266,001 to $334,000:

- Medicare Part B premium — $370.00 per month

- Medicare Part D IRMAA — $35.30 additional per month

Tier 4 — Third Medicare Income Limit Threshold 2026 Individual income $167,001 to $200,000 or joint $334,001 to $400,000:

- Medicare Part B premium — $480.90 per month

- Medicare Part D IRMAA — $57.00 additional per month

Tier 5 — Fourth Medicare Income Limit Threshold 2026 Individual income $200,001 to $500,000 or joint $400,001 to $750,000:

- Medicare Part B premium — $591.90 per month

- Medicare Part D IRMAA — $78.60 additional per month

Tier 6 — Highest Medicare Income Limit Tier 2026 Individual income above $500,000 or joint above $750,000:

- Medicare Part B premium — $628.90 per month

- Medicare Part D IRMAA — $85.80 additional per month

The difference between the standard Medicare income limit tier and the highest tier is enormous. A senior at the highest Medicare income limit tier in 2026 pays $628.90 per month for Part B compared to $185.00 for someone at or below the standard Medicare income limit — that is $443.90 more per month or $5,326.80 more per year.

How Are the Medicare Income Limits in 2026 Determined?

The Medicare income limits in 2026 are determined by the Social Security Administration using your Modified Adjusted Gross Income from your 2024 federal income tax return. Here is exactly how the Medicare income limits in 2026 are calculated:

Step 1 — The Social Security Administration accesses your 2024 tax return data from the IRS.

Step 2 — SSA calculates your MAGI by adding your Adjusted Gross Income plus any tax-exempt interest income.

Step 3 — SSA compares your MAGI to the Medicare income limits in 2026.

Step 4 — If your income exceeds the standard Medicare income limit SSA notifies you of your IRMAA surcharge amount by mail.

Step 5 — The IRMAA surcharge is added to your Medicare Part B and Part D premiums automatically.

The Medicare income limits in 2026 are indexed to inflation and adjusted annually. This means the income thresholds that define each Medicare income limit bracket change slightly each year.

What Income Counts Toward the Medicare Income Limits in 2026?

Understanding which income counts toward the Medicare income limits in 2026 helps you plan your finances and potentially reduce your Medicare costs.

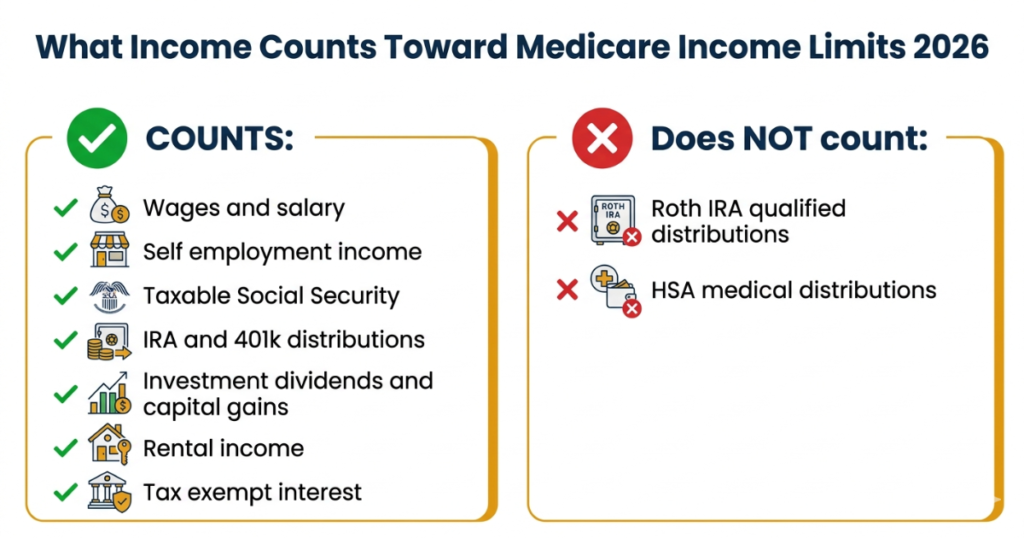

Your Modified Adjusted Gross Income for Medicare income limits purposes in 2026 includes:

- Wages and salary from employment

- Self-employment income — business profits and freelance income

- Taxable portion of Social Security benefits — 50% to 85% of benefits for most recipients

- Traditional IRA and 401(k) distributions

- Pension and annuity income

- Investment income — dividends, interest, and capital gains

- Rental income

- Tax-exempt interest from municipal bonds

Income that does NOT count toward the Medicare income limits in 2026:

- Qualified Roth IRA distributions — this is one of the biggest tax planning advantages of Roth accounts for Medicare-eligible seniors

- HSA distributions used for qualified medical expenses

- Life insurance proceeds

- Gifts and inheritances

Medicare Income Limits 2026 — Common Triggers for IRMAA

Many seniors are surprised to exceed the Medicare income limits in 2026 due to one-time income events that occurred in 2024. The most common triggers include:

Large IRA or 401(k) distributions — taking a large retirement account withdrawal in 2024 can push your income over the Medicare income limits in 2026 even if your regular annual income is well below the threshold.

Roth IRA conversions — converting a traditional IRA to a Roth IRA generates taxable income that counts toward the Medicare income limits in 2026. Large Roth conversions done in 2024 may result in IRMAA surcharges in 2026.

Sale of real estate or investments — capital gains from selling a home, investment property, or stocks in 2024 can temporarily push your income over the Medicare income limits in 2026.

Required Minimum Distributions — seniors who turned 73 in 2024 were required to start taking RMDs from retirement accounts. Large RMDs can push income over the Medicare income limits.

Pension lump sum payments — receiving a pension buyout or lump sum in 2024 counts toward the Medicare income limits in 2026.

The good news is these are often one-time events. If your 2025 income is below the Medicare income limits your IRMAA surcharges will be reduced in 2027 when your premium is recalculated.

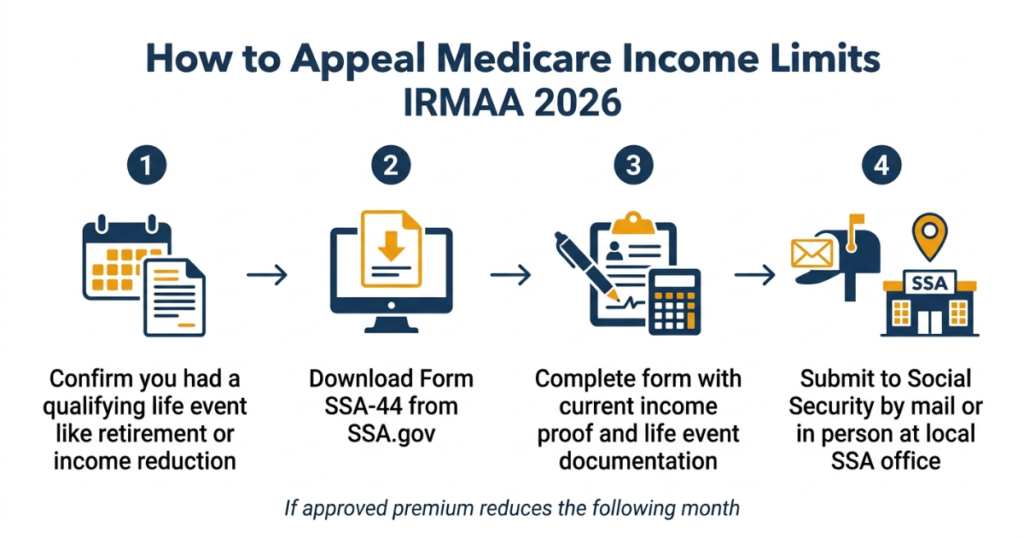

How to Appeal the Medicare Income Limits Surcharge in 2026

If you are paying IRMAA surcharges due to exceeding the Medicare income limits in 2026 and your income has since decreased you have the right to appeal. You can appeal the Medicare income limits IRMAA surcharge if you experienced one of these qualifying life-changing events:

- Marriage

- Divorce or legal separation

- Death of a spouse

- Work stoppage or retirement

- Work reduction — reduced hours or salary

- Loss of income-producing property due to disaster

- Loss of pension income

- Employer settlement payment

To appeal the Medicare income limits IRMAA surcharge in 2026 file Form SSA-44 with the Social Security Administration. Download Form SSA-44 from SSA.gov or pick it up at your local Social Security office.

When filing your Medicare income limits appeal include documentation of the qualifying life event such as a retirement letter, documentation of your current income, and your most recent tax return showing lower income.

After reviewing your appeal the Social Security Administration will recalculate your premium based on your current income. If approved your Medicare Part B and Part D premiums will be reduced effective the following month.

Strategies to Reduce Your Medicare Costs Near the Income Limits

If your income is near the Medicare income limits in 2026 there are legitimate strategies that may help you stay below the thresholds:

Strategy 1 — Use Roth IRA instead of traditional IRA distributions Qualified Roth IRA distributions do not count toward the Medicare income limits in 2026. Drawing from your Roth first can keep your MAGI below the Medicare income limits.

Strategy 2 — Qualified Charitable Distributions If you are 70.5 or older you can make Qualified Charitable Distributions directly from your IRA to charity up to $105,000 per year in 2026. QCDs satisfy your RMD requirement without counting toward your MAGI — helping you stay below the Medicare income limits in 2026.

Strategy 3 — Manage capital gains timing Spreading large capital gains realizations across multiple years can help you stay below the Medicare income limit thresholds.

Strategy 4 — Plan Roth conversions carefully When doing Roth IRA conversions keep your total income including the conversion amount below the Medicare income limit thresholds to avoid IRMAA surcharges.

Strategy 5 — Work with a financial advisor A financial advisor who understands the Medicare income limits in 2026 can help you optimize your income strategy to minimize IRMAA surcharges in retirement.

Medicare Income Limits 2026 — Married Filing Separately

Seniors who are married and file their taxes separately face much stricter Medicare income limits in 2026. If you are married filing separately the Medicare income limits in 2026 are dramatically harsher:

- Income up to $106,000 — standard premium $185.00 per month

- Income above $106,000 — immediately jumps to $628.90 per month — the maximum tier

There is no middle ground for married filing separately under the Medicare income limits. Any income above $106,000 immediately triggers the maximum IRMAA surcharge. This is why tax advisors typically recommend married couples file jointly to take advantage of the more favorable Medicare income limit thresholds.

Frequently Asked Questions — Medicare Income Limits 2026

What are the Medicare income limits in 2026?

The standard Medicare income limit in 2026 is $106,000 for individuals and $212,000 for married couples filing jointly. If your 2024 Modified Adjusted Gross Income was at or below these Medicare income limits you pay the standard Part B premium of $185.00 per month. If your income exceeded the Medicare income limits in 2026 you pay IRMAA surcharges ranging from $259.00 to $628.90 per month depending on your income tier.

How do I know if I exceed the Medicare income limits in 2026?

The Social Security Administration automatically determines whether your income exceeds the Medicare income limits in 2026 using your 2024 tax return data from the IRS. If you exceed the Medicare income limits SSA will send you an IRMAA determination letter explaining your higher premium. You do not need to self-report your income to Medicare.

Can I lower my Medicare premium if I exceeded the income limits due to a one-time event?

Yes. If you exceeded the Medicare income limits in 2026 due to a one-time income event such as a large IRA withdrawal or property sale and your current income is below the limits you can appeal your IRMAA surcharge by filing Form SSA-44 with the Social Security Administration.

Do Roth IRA withdrawals count toward the Medicare income limits in 2026?

No. Qualified Roth IRA distributions do not count toward your MAGI for Medicare income limit purposes in 2026. This is one of the main advantages of Roth retirement accounts for Medicare-eligible seniors — using Roth distributions instead of traditional IRA withdrawals can help you stay below the Medicare income limits and avoid IRMAA surcharges.

Do Social Security benefits count toward the Medicare income limits in 2026?

Yes — the taxable portion of your Social Security benefits counts toward your MAGI for Medicare income limit purposes in 2026. For most Social Security recipients between 50% and 85% of their benefit is taxable and included in the MAGI calculation for the Medicare income limits.

What happens if my income drops below the Medicare income limits next year?

If your income drops below the Medicare income limits in a future year your IRMAA surcharges will be reduced or eliminated in the year two years after the lower income year. For example if your 2025 income is below the standard Medicare income limit your 2027 Medicare premium will be at the standard rate of $185.00 per month.

Are the Medicare income limits the same for Part B and Part D?

The Medicare income limit thresholds are the same for both Part B and Part D in 2026. However the IRMAA surcharge amounts differ — Part B surcharges range from $74 to $443.90 additional per month while Part D surcharges range from $13.70 to $85.80 additional per month.

Summary — Medicare Income Limits 2026

The Medicare income limits in 2026 determine whether you pay the standard $185.00 per month Medicare Part B premium or higher IRMAA surcharges. The standard Medicare income limit in 2026 is $106,000 for individuals and $212,000 for joint filers. Seniors above the Medicare income limits pay between $259.00 and $628.90 per month for Part B depending on their income tier.

The Medicare income limits in 2026 are based on your 2024 MAGI and automatically calculated by the Social Security Administration. If your income has decreased since 2024 due to a qualifying life event you can appeal your IRMAA surcharge by filing Form SSA-44. Strategic tax planning — particularly using Roth IRA distributions and Qualified Charitable Distributions — can help you stay below the Medicare income limits and avoid IRMAA surcharges.

For free personalized help understanding how the Medicare income limits in 2026 affect your situation contact your State Health Insurance Assistance Program (SHIP) counselor at shiphelp.org or call Medicare free at 1-800-633-4227.

This guide is for informational purposes only and is not financial or tax advice. Always verify current Medicare income limits at Medicare.gov and consult a qualified financial advisor for personalized income planning guidance.

Sources: Medicare.gov | CMS.gov | SSA.gov | AARP.org

Last updated: April 2026 | Author: James Carter, Independent Medicare Research Analyst

For hottest information you have to go to see web and

on internet I found this website as a finest site for most up-to-date updates.