Medicare Advantage vs Medigap — Which is Better in 2026?

Medicare Advantage vs Medigap — which is better in 2026? This is the single most important Medicare decision most seniors will ever make. Choosing between Medicare Advantage vs Medigap affects your monthly premiums, your out-of-pocket costs, which doctors you can see, and what extra benefits you receive. In this complete 2026 guide we break down everything you need to know about Medicare Advantage vs Medigap — costs, coverage, pros and cons, and exactly which option works best for different types of seniors. All information is sourced from Medicare.gov and CMS.gov.

ALSO READ- Medicare Part A vs Part B — What Is the Difference in 2026? Also Read- Aetna Medicare Advantage Plans 2026 — Complete Review

What You Will Learn — Medicare Advantage vs Medigap

- The key difference between Medicare Advantage vs Medigap

- How Medicare Advantage works in 2026

- How Medigap works in 2026

- Cost comparison — Medicare Advantage vs Medigap

- Coverage comparison — Medicare Advantage vs Medigap

- Pros and cons of Medicare Advantage vs Medigap

- Which is better for different types of seniors

- How to switch between Medicare Advantage and Medigap

- Frequently asked questions about Medicare Advantage vs Medigap

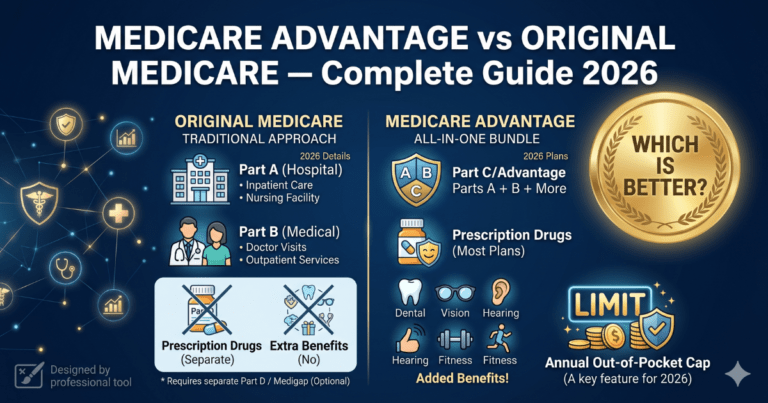

Medicare Advantage vs Medigap — The Key Difference

Before diving into the full Medicare Advantage vs Medigap comparison it is important to understand what each option actually is.

Medicare Advantage (Part C) is a complete replacement for Original Medicare. Instead of the federal government paying your Medicare claims directly a private insurance company approved by Medicare manages all your coverage. Medicare Advantage plans must cover everything Original Medicare covers and most plans include extra benefits like dental, vision, hearing, and prescription drugs.

Medigap (also called Medicare Supplement insurance) works differently. With Medigap you keep Original Medicare (Parts A and B) as your primary insurance and the Medigap plan acts as a secondary insurance that fills in the gaps — paying the deductibles, coinsurance, and copayments that Original Medicare leaves you responsible for.

The fundamental difference between Medicare Advantage vs Medigap is this — Medicare Advantage replaces Original Medicare while Medigap supplements it.

How Medicare Advantage Works in 2026

Medicare Advantage plans are offered by private insurance companies like Humana, UnitedHealthcare, Aetna, and Cigna that are approved and regulated by Medicare. When you enroll in Medicare Advantage you are still technically enrolled in Medicare — but your benefits are delivered through the private plan instead of through the federal government directly.

Medicare Advantage plans in 2026 come in several types:

Health Maintenance Organization (HMO) plans require you to use a network of local doctors and hospitals. You usually need a referral from your primary care doctor to see a specialist. HMO plans typically have lower premiums but less flexibility in choosing providers.

Preferred Provider Organization (PPO) plans give you more flexibility to see doctors and hospitals both inside and outside the plan network. You pay less when you use in-network providers but can still see out-of-network providers at higher cost. PPO plans usually have slightly higher premiums than HMO plans.

Private Fee-for-Service (PFFS) plans determine how much they will pay doctors and hospitals and how much you pay when you receive services. You can see any Medicare-approved provider who agrees to the plan’s payment terms.

Special Needs Plans (SNPs) are designed for people with specific diseases or characteristics such as people with diabetes, heart disease, or people who live in nursing homes. SNPs tailor their benefits, provider choices, and drug formularies to best serve their specific members.

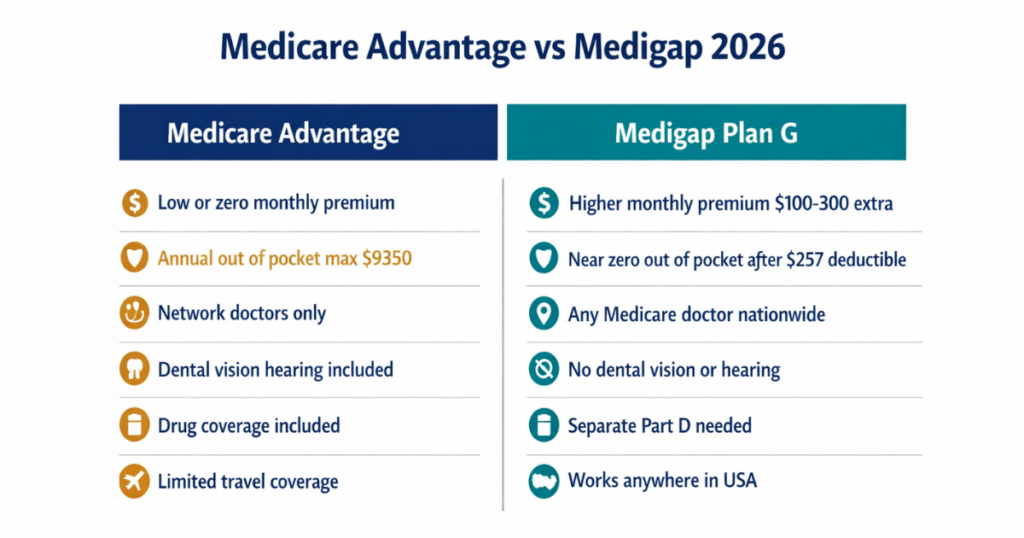

Key features of Medicare Advantage plans in 2026 include an annual out-of-pocket maximum of $9,350 which provides important financial protection. Once you reach this limit the plan pays 100% of covered services for the rest of the year. Original Medicare has no out-of-pocket maximum — meaning without a supplement your costs could theoretically be unlimited.

How Medigap Works in 2026

Medigap plans are standardized supplemental insurance policies sold by private insurance companies to fill the coverage gaps in Original Medicare. There are 10 standardized Medigap plans labeled A through N. Every insurance company selling Medigap must offer the same standardized benefits for each plan letter — so Medigap Plan G from Humana offers the exact same coverage as Plan G from Aetna. The only difference is price.

The most popular Medigap plans in 2026 are:

Medigap Plan G is the most popular plan for new Medicare enrollees in 2026. It covers the Medicare Part A deductible ($1,676), Part A coinsurance and hospital costs, Part B coinsurance (20%) after you pay the Part B deductible ($257), skilled nursing facility coinsurance, foreign travel emergency coverage up to plan limits, and Part A hospice care coinsurance. Plan G does not cover the annual Part B deductible of $257 — that is the only gap.

Medigap Plan N is the second most popular option. It covers the same benefits as Plan G except you pay up to $20 for some doctor visits and up to $50 for emergency room visits that do not result in an inpatient admission. Plan N premiums are typically 15% to 25% lower than Plan G premiums making it attractive for healthier seniors who visit doctors infrequently.

Medigap Plan F was the most comprehensive plan available but it is no longer available to people who became eligible for Medicare on or after January 1 2020. If you were eligible before that date you may still be able to buy Plan F.

With any Medigap plan you keep full Original Medicare coverage — meaning you can see any doctor or hospital in the United States that accepts Medicare with no network restrictions.

Medicare Advantage vs Medigap — Cost Comparison 2026

The cost comparison between Medicare Advantage vs Medigap is one of the most important factors in the decision. Here is the complete cost breakdown for 2026:

Monthly Premium Comparison

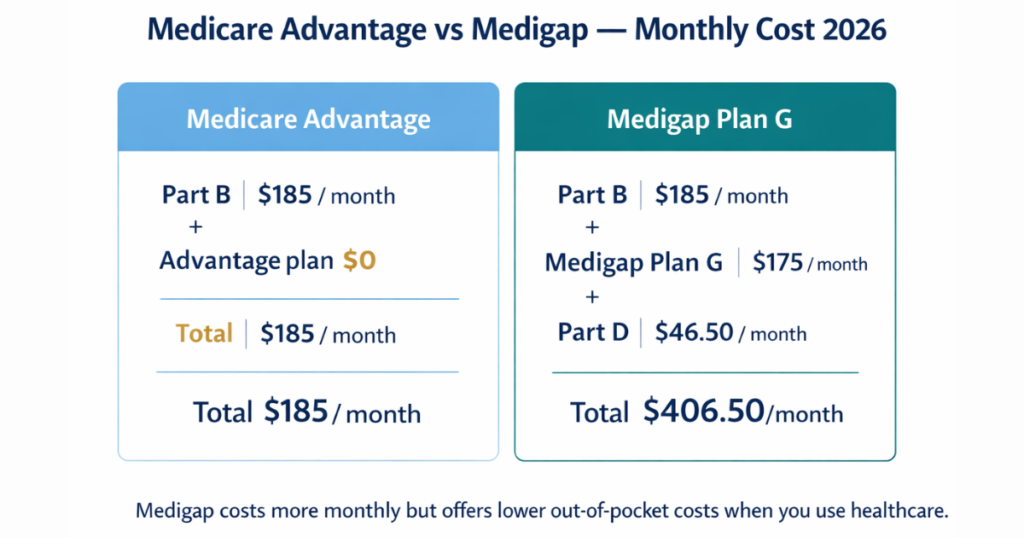

Medicare Advantage monthly cost:

- Part B premium — $185.00 per month (everyone pays this)

- Medicare Advantage plan premium — $0 for many plans

- Total monthly cost — as low as $185.00 per month

- Some plans charge $20 to $100 additional premium

Medigap monthly cost:

- Part B premium — $185.00 per month

- Medigap Plan G premium — $100 to $300 per month average

- Part D drug plan — $46.50 per month average

- Total monthly cost — $331.50 to $531.50 per month

Medicare Advantage wins on monthly premium. Most Medicare Advantage plans have $0 additional premium beyond the Part B premium you already pay. Medigap plus Part D typically costs $150 to $350 more per month than Medicare Advantage.

Out-of-Pocket Cost Comparison

Medicare Advantage:

- Annual out-of-pocket maximum — $9,350 in 2026

- After reaching maximum — plan pays 100%

- Copays and coinsurance apply for each service used

- Typical doctor visit copay — $5 to $45

- Typical specialist visit copay — $20 to $80

- Typical hospital stay — $250 to $500 per day

- Annual out-of-pocket maximum — effectively $257 (just the Part B deductible)

- After paying $257 deductible — Plan G covers 100% of Part A and Part B costs

- No copays for covered services after deductible

- No coinsurance for covered services after deductible

- Highly predictable costs year after year

Medigap wins on out-of-pocket costs and predictability. Once you pay the $257 Part B deductible Medigap Plan G covers everything else — giving you near-zero out-of-pocket costs for the rest of the year.

Annual Total Cost Comparison Example

For a senior with average healthcare usage in 2026:

Medicare Advantage (HMO with $0 premium):

- Monthly premiums — $185 Part B only = $2,220 per year

- Out-of-pocket costs (average usage) — $500 to $1,500 per year

- Total annual cost estimate — $2,720 to $3,720 per year

Original Medicare plus Medigap Plan G plus Part D:

- Monthly premiums — $185 + $175 Medigap + $46.50 Part D = $406.50 per month = $4,878 per year

- Out-of-pocket costs (just Part B deductible) — $257 per year

- Total annual cost estimate — $5,135 per year

For healthy seniors with low healthcare usage Medicare Advantage is often significantly cheaper. For seniors with frequent medical needs and high healthcare costs Medigap often provides better financial protection because your costs are capped at the $257 deductible with Plan G.

Medicare Advantage vs Medigap — Coverage Comparison 2026

Doctor and Hospital Choice

Medicare Advantage — you must use the plan’s network of local doctors and hospitals. Going out of network costs more or may not be covered at all depending on your plan type. If your preferred doctor is not in the plan network you cannot see them without paying full price.

Medigap — you can see any doctor or hospital in the United States that accepts Medicare. There are no networks and no referrals required. This is ideal for seniors who travel frequently or want complete freedom of choice.

Extra Benefits

Medicare Advantage — most plans include dental, vision, and hearing benefits that Original Medicare does not cover. Many plans also include fitness memberships like SilverSneakers, over-the-counter allowances, transportation to medical appointments, and meal delivery after hospital stays.

Medigap — covers none of the extra benefits. You have no dental, vision, or hearing coverage from your Medigap plan. You would need to buy separate standalone dental and vision insurance which adds to your monthly premium costs.

Prescription Drug Coverage

Medicare Advantage — drug coverage is usually included in Medicare Advantage Prescription Drug (MAPD) plans at no additional premium.

Medigap — does not include prescription drug coverage. You must buy a separate Medicare Part D drug plan at an average cost of $46.50 per month.

Travel Coverage

Medicare Advantage — most plans only work within their local service area. If you travel to another state or country and need medical care you typically only have coverage for emergency and urgent care situations.

Medigap — works anywhere in the United States. Medigap Plan G also includes foreign travel emergency coverage for the first 60 days of a trip after a $250 deductible up to plan limits. This is significant for seniors who travel internationally.

Medicare Advantage vs Medigap — Pros and Cons

Medicare Advantage Pros

- Lower monthly premiums — often $0 beyond Part B premium

- Annual out-of-pocket maximum protects against catastrophic costs

- Extra benefits — dental, vision, hearing usually included

- Drug coverage usually included — no need for separate Part D

- Simple all-in-one coverage from one insurance company

Medicare Advantage Cons

- Restricted to plan network of local doctors and hospitals

- Referrals usually required to see specialists

- Coverage varies by zip code — plans change annually

- May need prior authorization for some procedures

- Less predictable costs — copays apply for each service

- Limited coverage when traveling outside service area

- Plan can change benefits or leave your area each year

Medigap Pros

- Complete freedom to see any Medicare-accepting doctor or hospital nationwide

- No referrals needed for any specialist

- Highly predictable out-of-pocket costs — especially with Plan G

- Works anywhere in the US — ideal for travelers and snowbirds

- Coverage never changes — standardized benefits are guaranteed

- Insurance company cannot drop you as long as you pay premiums

Medigap Cons

- Higher monthly premiums than Medicare Advantage

- No extra benefits — no dental, vision, or hearing coverage

- Must buy separate Part D drug plan at additional cost

- Medical underwriting may apply if you enroll outside open enrollment

- More complex — managing multiple insurance policies

Which is Better — Medicare Advantage or Medigap?

The Medicare Advantage vs Medigap decision depends entirely on your personal situation. There is no single right answer for every senior. Here is a guide to help you decide which is better for your specific circumstances:

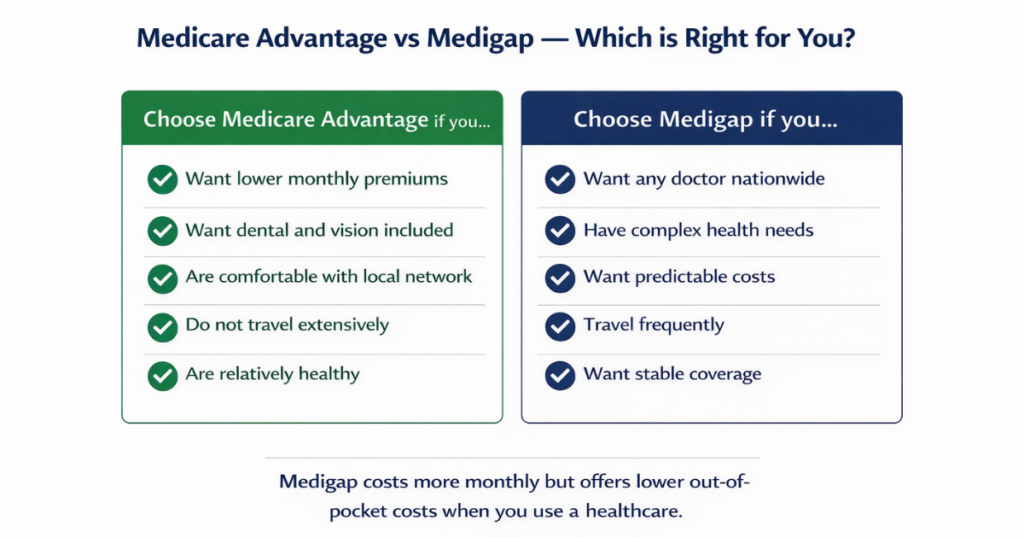

Medicare Advantage may be better for you if:

- You want to minimize monthly premiums

- You want dental, vision, and hearing coverage included

- You are relatively healthy with infrequent medical needs

- You are comfortable using a local network of doctors

- You do not travel extensively

- You live in an area with high-quality Medicare Advantage plans

- Your preferred doctors are in the plan network

Medigap may be better for you if:

- You want complete freedom to see any doctor or hospital nationwide

- You have complex medical needs requiring frequent specialist visits

- You want predictable out-of-pocket costs with no surprise bills

- You travel frequently or split time between states

- You have ongoing health conditions requiring regular treatment

- You value stability — your coverage never changes year to year

- You can afford slightly higher monthly premiums

The most important questions to ask yourself:

Are my current doctors in the Medicare Advantage plan network? If your trusted doctors are not in-network Medicare Advantage may force you to switch providers.

How often do I use medical services? Healthy seniors with low healthcare usage often do better financially with Medicare Advantage. Seniors with frequent medical needs often save money with Medigap despite higher premiums.

Do I travel frequently? Snowbirds and frequent travelers generally prefer Medigap because it works anywhere in the US.

How important is dental and vision coverage to me? If dental and vision are important Medicare Advantage often provides these at no extra cost.

How to Switch Between Medicare Advantage and Medigap

Understanding how to switch between Medicare Advantage vs Medigap is important before you make your initial choice.

Switching from Medigap to Medicare Advantage

You can switch from Medigap to Medicare Advantage during the Annual Open Enrollment Period (October 15 to December 7) or the Medicare Advantage Open Enrollment Period (January 1 to March 31). You simply enroll in a Medicare Advantage plan and your Medigap plan ends automatically.

Switching from Medicare Advantage back to Medigap

This is more difficult. When switching from Medicare Advantage back to Original Medicare with Medigap in most states insurance companies can use medical underwriting — meaning they can charge you higher premiums or deny you coverage based on your health history. The exception is if you are in your Medigap Open Enrollment Period (the 6 months starting when you first enroll in Part B at age 65) or have a guaranteed issue right due to a specific qualifying event.

This asymmetry is one of the most important things to understand in the Medicare Advantage vs Medigap decision. It is generally easier to switch from Medigap to Medicare Advantage than the other way around. If you start with Medicare Advantage and later want Medigap you may face medical underwriting challenges in most states. Note that a few states — New York, Massachusetts, Connecticut, Maine, and a handful of others — have their own rules that may allow year-round Medigap enrollment regardless of health status.

Frequently Asked Questions — Medicare Advantage vs Medigap

Is Medicare Advantage the same as Medigap?

No. Medicare Advantage and Medigap are completely different types of Medicare coverage. Medicare Advantage (Part C) replaces Original Medicare with an all-in-one plan from a private insurance company. Medigap supplements Original Medicare by filling in the coverage gaps like deductibles and coinsurance. They work in completely different ways and you cannot have both at the same time.

Can I have both Medicare Advantage and Medigap?

No. You cannot have Medicare Advantage and Medigap at the same time. If you are enrolled in Medicare Advantage it is illegal for an insurance company to sell you a Medigap policy. They are mutually exclusive options.

Which is cheaper — Medicare Advantage or Medigap?

Medicare Advantage typically has lower monthly premiums — often $0 beyond the Part B premium of $185 per month. Medigap plus Part D typically costs $150 to $350 more per month. However Medigap has lower and more predictable out-of-pocket costs when you actually use healthcare services. The total annual cost comparison between Medicare Advantage vs Medigap depends on your health status and how often you use medical services.

Does Medicare Advantage cover more than Medigap?

Medicare Advantage often includes extra benefits like dental, vision, hearing, and drug coverage that Medigap does not include. However Medigap provides more comprehensive coverage for your Part A and Part B costs — nearly eliminating out-of-pocket expenses for covered services with Plan G. The answer depends on which type of coverage you prioritize.

What happens to my Medigap plan if I switch to Medicare Advantage?

If you switch from Medigap to Medicare Advantage your Medigap policy is no longer needed and you should cancel it. You should not continue paying Medigap premiums while enrolled in Medicare Advantage as the plans do not work together.

When is the best time to sign up for Medigap?

The best time to sign up for Medigap is during your Medigap Open Enrollment Period — the 6-month period that begins the month you are both 65 or older and enrolled in Medicare Part B. During this period you have guaranteed issue rights meaning insurance companies cannot deny you coverage or charge you more based on your health status.

Can Medicare Advantage plans change their benefits each year?

Yes. Medicare Advantage plans can change their premiums, copays, covered drugs, network of providers, and extra benefits each year during the Annual Notice of Change period. This is one of the key differences in the Medicare Advantage vs Medigap comparison — Medigap benefits are standardized and cannot change once you enroll.

Which do doctors prefer — Medicare Advantage or Medigap?

Many doctors prefer patients with Original Medicare plus Medigap because they receive full Medicare reimbursement with no network restrictions or prior authorization requirements. Some doctors do not accept all Medicare Advantage plans. Always confirm your preferred doctors accept your specific Medicare Advantage plan before enrolling.

Summary — Medicare Advantage vs Medigap

The Medicare Advantage vs Medigap decision is one of the most personal financial decisions you will make as you approach retirement. There is no universally correct answer — the right choice depends entirely on your health, your finances, your doctors, and your lifestyle.

Medicare Advantage wins on monthly premiums, extra benefits, and simplicity. Medigap wins on doctor choice, predictable costs, and stability. Choosing between Medicare Advantage vs Medigap means deciding which of these factors matters most to you personally.

Use the free plan comparison tool at Medicare.gov to compare specific Medicare Advantage plans available in your zip code. For free unbiased help contact your State Health Insurance Assistance Program (SHIP) counselor at shiphelp.org or call Medicare free at 1-800-633-4227.

This guide is for informational purposes only and is not medical or financial advice. Always verify current Medicare plan details at Medicare.gov before making enrollment decisions.

Sources: Medicare.gov | CMS.gov | SSA.gov | AARP.org | KFF.org

Last updated: April 2026 | Author: James Carter, Independent Medicare Research Analyst

12 Comments