How Does Medicare Work for Seniors — Complete Guide 2026

How does Medicare work for seniors? If you are turning 65 or helping an elderly parent navigate health insurance for the first time — this guide answers everything. Medicare is the federal health insurance program for Americans aged 65 and older covering more than 65 million seniors across the United States. In this complete 2026 guide we break down exactly how Medicare works for seniors — Parts A, B, C and D, costs, enrollment deadlines and how to avoid costly mistakes. All information is sourced directly from Medicare.gov and CMS.gov.

How Does Medicare Work for Seniors?

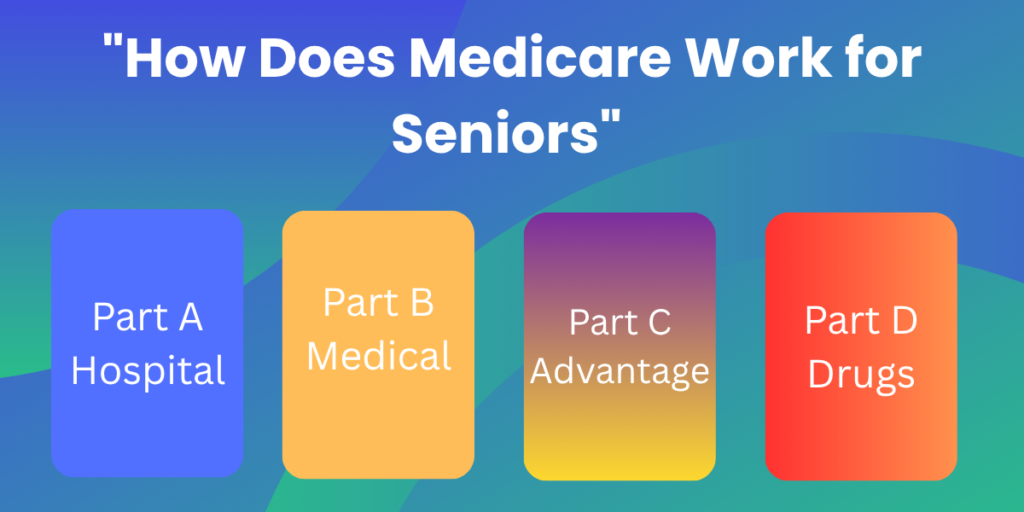

Medicare works by dividing your health coverage into four parts — Part A, Part B, Part C and Part D. Each part covers different medical services. Most seniors use a combination of these parts to get complete health coverage.

Here is how Medicare works for seniors step by step:

- You enroll in Medicare Part A and Part B — called Original Medicare

- Part A covers hospital stays and inpatient care

- Part B covers doctor visits and outpatient services

- You then choose either a Medigap supplement or Medicare Advantage plan

- You add Part D for prescription drug coverage if needed

Understanding how each part works is the most important step in choosing the right Medicare coverage for your situation.

Who Is Medicare For?

Medicare is designed specifically for seniors aged 65 and older. However certain younger Americans also qualify. You are eligible for Medicare if you meet one of the following criteria:

- You are aged 65 or older and a US citizen or permanent legal resident who has lived in the US for at least 5 continuous years

- You are under 65 and have received Social Security Disability Insurance (SSDI) for at least 24 months

- You have End-Stage Renal Disease (ESRD) — permanent kidney failure requiring dialysis or a kidney transplant

- You have been diagnosed with ALS (Lou Gehrig’s disease) — Medicare begins immediately upon diagnosis

Most seniors become eligible for Medicare at age 65 regardless of whether they are still working or already retired. You do not need to be receiving Social Security benefits to enroll in Medicare.

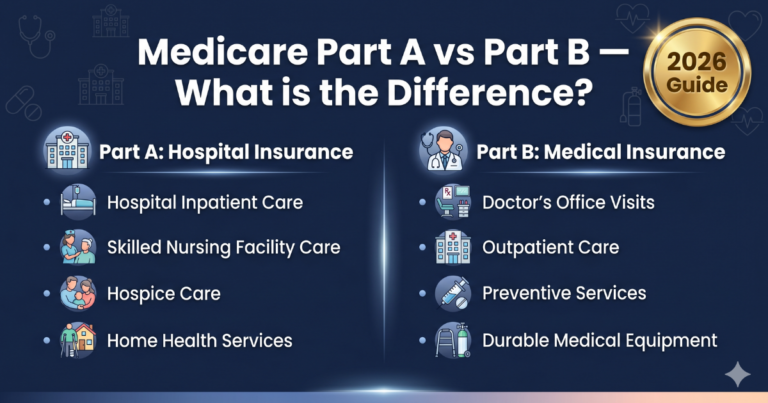

Medicare Part A — How Does Hospital Coverage Work for Seniors?

Medicare Part A is your hospital insurance. It covers the cost of inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care services.

Most seniors pay $0 per month for Part A if they or their spouse worked and paid Medicare taxes for at least 10 years (40 quarters). If you did not work long enough you can still buy Part A but you will pay a monthly premium of up to $505 per month in 2026.

What Part A covers in 2026:

- Hospital stay days 1–60 — $1,676 deductible per benefit period

- Hospital stay days 61–90 — $419 per day coinsurance

- Hospital stay days 91 and beyond — $838 per day lifetime reserve days

- Skilled nursing facility days 1–20 — $0

- Skilled nursing facility days 21–100 — $209.50 per day

- Skilled nursing facility days 100+ — you pay 100% of costs

- Hospice care — $0 for most services

- Home health care — $0 for approved services

Important: Part A does not cover long-term custodial care in a nursing home. It only covers short-term skilled nursing care after a qualifying hospital stay of at least 3 days.

Medicare Part B — How Does Medical Coverage Work for Seniors?

Medicare Part B is your medical insurance. It covers outpatient medical services including doctor visits, preventive care screenings, lab tests, X-rays, mental health services, and durable medical equipment like wheelchairs and walkers.

Unlike Part A, everyone pays a monthly premium for Part B. The standard Part B premium in 2026 is $185.00 per month. Higher income seniors pay more — this is called IRMAA (Income Related Monthly Adjustment Amount).

What Part B covers in 2026:

- Standard monthly premium — $185.00 per month

- Annual deductible — $257 per year

- Doctor visits and outpatient services — you pay 20% after deductible

- Preventive screenings — $0 fully covered including mammograms, colonoscopies and annual wellness visits

- Mental health services — 20% after deductible

- Durable medical equipment — 20% after deductible

- Lab tests and X-rays — 20% after deductible

- Ambulance services — 20% after deductible

Higher income seniors pay more for Part B. If your individual income is above $106,000 or your joint income is above $212,000 you will pay a higher premium in 2026. The maximum Part B premium for high earners is $628.90 per month in 2026.

Always verify current Part B premiums at Medicare.gov as these change every January.

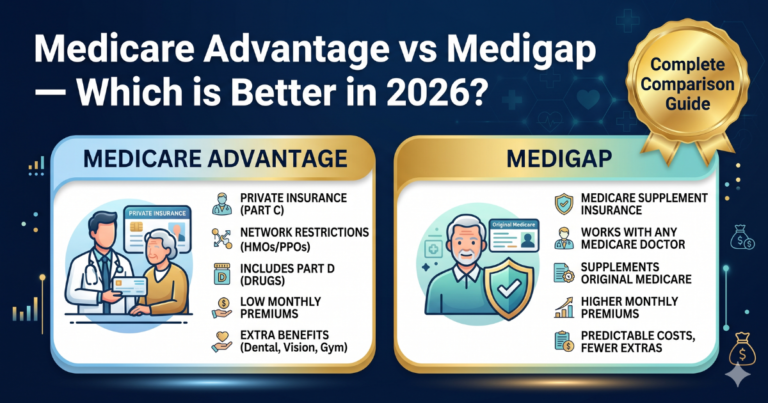

Medicare Part C — How Does Medicare Advantage Work for Seniors?

Medicare Part C is also called Medicare Advantage. It is an alternative way to receive your Medicare benefits through a private insurance company that is approved and regulated by Medicare.

Medicare Advantage plans must cover everything that Original Medicare Parts A and B cover. Most plans also include additional benefits that Original Medicare does not cover — including dental care, vision care, hearing aids, and prescription drug coverage.

How Medicare Advantage works for seniors:

- You still pay your Part B premium of $185 per month

- Many Medicare Advantage plans charge $0 additional premium

- You see doctors within the plan’s network

- Most plans require referrals to see specialists

- Plans have an annual out-of-pocket maximum of $9,350 in 2026 — Original Medicare has no out-of-pocket limit

- Plans vary by county and zip code — not every plan is available everywhere

Medicare Advantage can be a good option for seniors who want extra benefits like dental and vision, want predictable costs with an out-of-pocket maximum, and are comfortable staying within a network of local doctors and hospitals.

Medicare Part D — How Does Drug Coverage Work for Seniors?

Medicare Part D covers prescription drugs. It is offered through private insurance companies approved by Medicare. Part D is optional but seniors who do not enroll when first eligible and do not have other qualifying drug coverage will face a permanent late enrollment penalty.

How Part D works for seniors in 2026:

- Average monthly premium — $46.50 per month

- Maximum annual deductible — $590

- Annual out-of-pocket maximum — $2,000 (new in 2025 — a major improvement for seniors)

- The coverage gap or donut hole was eliminated in 2024

If you have Original Medicare you need to buy a standalone Part D plan separately. If you have Medicare Advantage drug coverage is usually already included in your plan — called MAPD (Medicare Advantage Prescription Drug plan).

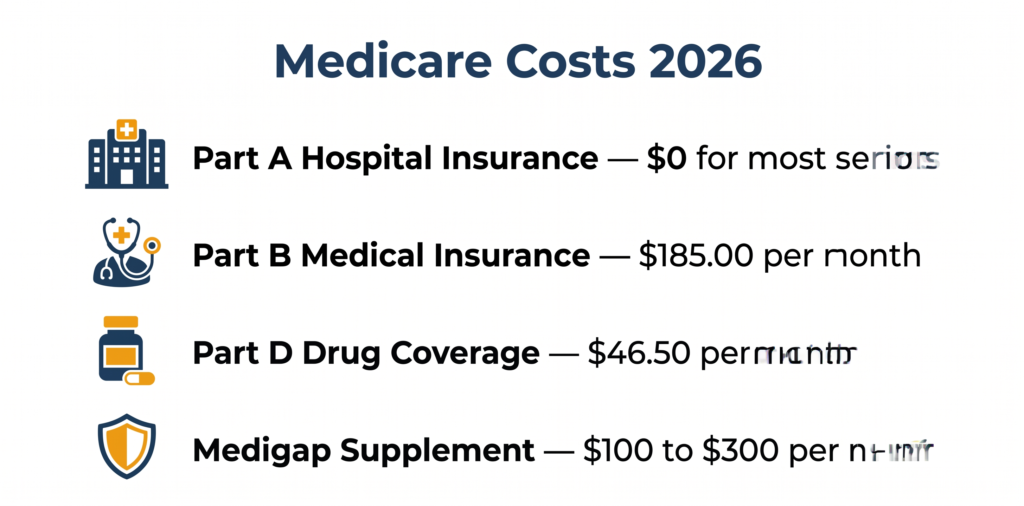

How Much Does Medicare Cost for Seniors in 2026?

One of the most common questions seniors ask is — how much does Medicare actually cost? The answer depends on which parts of Medicare you have, your income level, and how much healthcare you use during the year.

Full Medicare cost breakdown for seniors 2026:

- Part A premium — $0 for most seniors who worked 10+ years

- Part A deductible — $1,676 per benefit period

- Part B premium — $185.00 per month standard

- Part B deductible — $257 per year

- Part C (Medicare Advantage) premium — $0 to $100+ varies by plan

- Part D premium — $46.50 average per month

- Part D deductible — up to $590 per year

- Medigap supplement premium — $100 to $300+ per month varies by plan and state

The average senior on Original Medicare plus a Part D drug plan and no supplement pays approximately $231.50 per month in premiums in 2026 before any deductibles or coinsurance.

Seniors with Medicare Advantage often pay less in monthly premiums but may face higher costs when they actually use medical services depending on their plan.

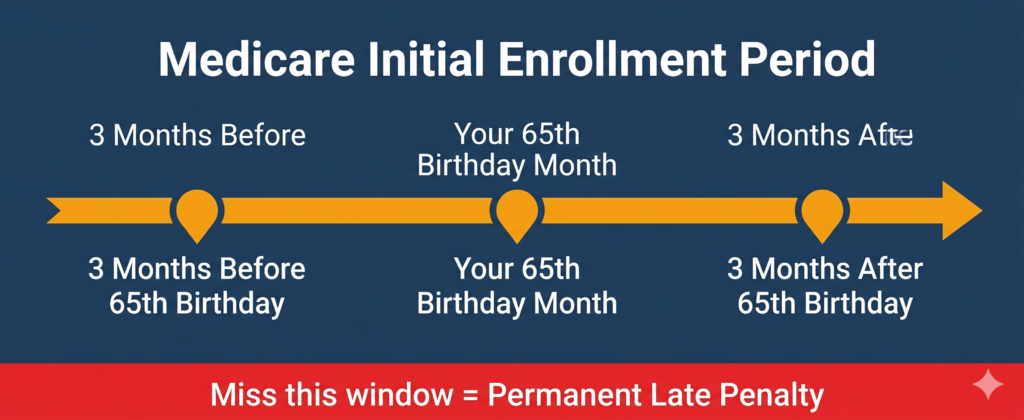

When Should Seniors Enroll in Medicare?

Knowing when to enroll in Medicare is critical. Missing your enrollment window can result in permanent late enrollment penalties that increase your premiums every single month for life.

Initial Enrollment Period (IEP)

Your Initial Enrollment Period is a 7-month window around your 65th birthday:

- 3 months before the month you turn 65

- The month you turn 65

- 3 months after the month you turn 65

This is the best time to enroll in Medicare Parts A and B. If you enroll in the first 3 months your coverage starts the first day of your birthday month. If you enroll in month 4, 5, 6 or 7 your coverage start date is delayed.

Annual Open Enrollment Period

Every year from October 15 to December 7 you can make changes to your Medicare coverage including:

- Switching from Original Medicare to Medicare Advantage

- Switching from Medicare Advantage back to Original Medicare

- Changing your Medicare Advantage plan

- Adding, dropping or changing your Part D drug plan

Changes made during Open Enrollment take effect January 1 of the following year.

Late Enrollment Penalties for Seniors

If you miss your Initial Enrollment Period without qualifying coverage from an employer you will face permanent late penalties:

- Part B late penalty — 10% added to your monthly premium for every 12 months you went without coverage — for life

- Part D late penalty — 1% of the national base premium per month you went without coverage — for life

These penalties never go away. A senior who delayed Part B enrollment by 2 years would pay 20% more every month for the rest of their life. Always enroll on time.

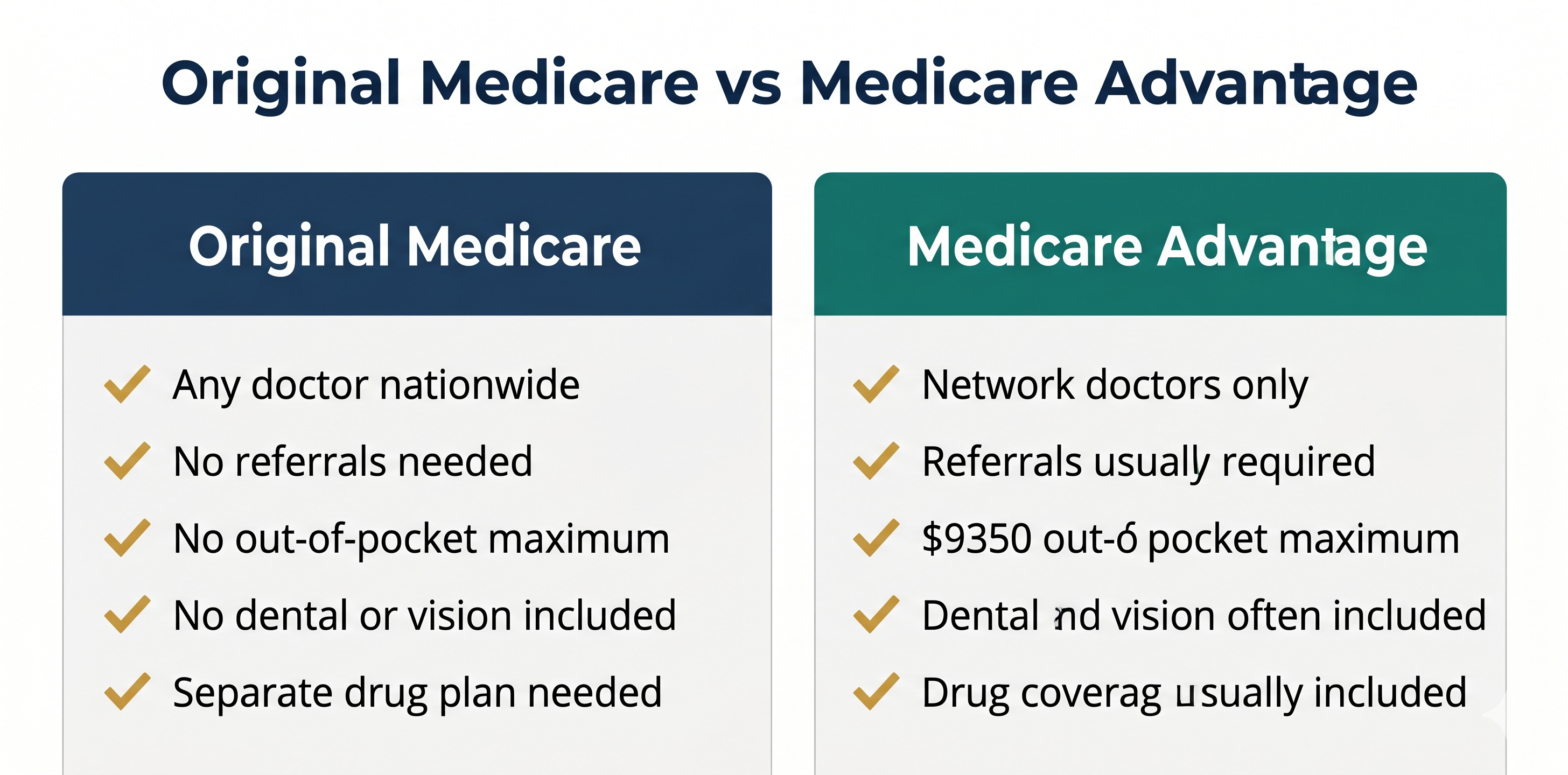

Original Medicare vs Medicare Advantage — Which Works Better for Seniors?

This is the most important Medicare decision most seniors will make. Here is a clear comparison:

Original Medicare:

- See any doctor or hospital in the US that accepts Medicare — no network restrictions

- No referrals needed to see specialists

- No annual out-of-pocket maximum — costs can be unlimited

- Does not cover dental, vision or hearing

- Need to buy separate Part D plan for drugs

- Need Medigap supplement to cover the 20% coinsurance gap

- Works nationwide — great for seniors who travel or have multiple residences

Medicare Advantage:

- Restricted to plan’s local network of doctors and hospitals

- Usually requires referrals for specialists

- Annual out-of-pocket maximum of $9,350 in 2026 — protects against catastrophic costs

- Most plans include dental, vision and hearing benefits

- Drug coverage usually included

- Often lower monthly premiums than Original Medicare plus Medigap

- Not ideal for seniors who travel frequently or want to see any doctor

Neither option is right for everyone. The best choice depends on your health, your doctors, your prescription drugs, and your budget. Use the free plan finder at Medicare.gov to compare plans available in your zip code.

What Does Medicare Cover for Seniors?

Original Medicare Parts A and B cover a wide range of medical services for seniors including:

- Inpatient hospital stays and surgery

- Doctor visits and specialist consultations

- Emergency and urgent care

- Preventive screenings — mammograms, colonoscopies, bone density tests, diabetes screenings

- Annual wellness visits — $0 with no copay

- Mental health services — inpatient and outpatient

- Physical therapy, occupational therapy and speech therapy

- Durable medical equipment — wheelchairs, walkers, CPAP machines

- Home health care — if homebound and meet Medicare criteria

- Hospice care for terminal illness

- Ambulance services

- Lab tests, X-rays and diagnostic imaging

- Some chiropractic care

- Diabetes self-management training

- Cardiac and pulmonary rehabilitation

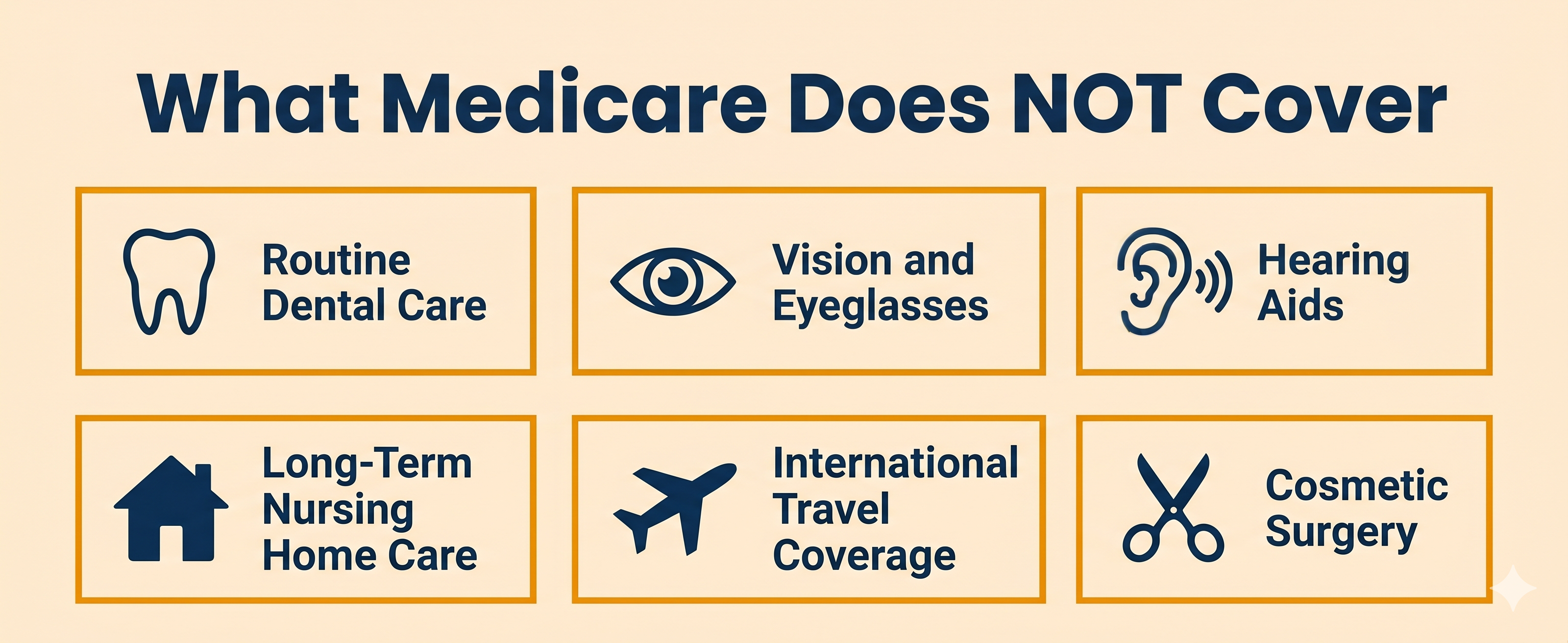

What Does Medicare NOT Cover for Seniors?

Original Medicare has significant coverage gaps. Medicare does NOT cover:

- Routine dental care — exams, cleanings, fillings, crowns, dentures

- Routine vision care — eye exams, prescription glasses, contact lenses

- Hearing aids and routine hearing exams

- Long-term custodial care in nursing homes or assisted living facilities

- Cosmetic surgery

- Most care received outside the United States

- Acupuncture — except for chronic low back pain

- Private duty nursing

- Personal care services — bathing, dressing, grooming

Many Medicare Advantage plans DO cover dental, vision and hearing benefits. If these are important to you compare Medicare Advantage plans carefully during Open Enrollment at Medicare.gov.

For long-term care needs consider speaking with a financial planner about long-term care insurance options as Medicare will not cover nursing home costs beyond 100 days How Does Medicare Work for Seniors — Complete Guide 2026.

How to Get Help Understanding Medicare as a Senior

Medicare can be confusing. Here are the best free resources for seniors:

- Medicare.gov — www.medicare.gov — official US Medicare website with plan finder tool

- 1-800-MEDICARE — call 1-800-633-4227 free 24 hours a day 7 days a week

- SHIP counselors — free unbiased local Medicare counseling at www.shiphelp.org — available in every state

- Social Security Administration — www.ssa.gov — for enrollment and eligibility questions

- State Medicaid office — if you have limited income you may qualify for programs that help pay Medicare costs

Frequently Asked Questions — How Does Medicare Work for Seniors?

Is Medicare free for seniors at age 65?

No. Medicare is not free for seniors. Most people pay $0 for Part A if they worked 10 or more years. But Part B costs $185 per month in 2026. You also pay deductibles and coinsurance when you use medical services. The total cost of Medicare for most seniors is $185 to $500+ per month depending on which coverage they choose.

How does Medicare work if I am still working at 65?

If you or your spouse are still actively working and covered by employer group health insurance you can delay Medicare enrollment without penalty. Once your employer coverage ends you have a Special Enrollment Period to sign up for Medicare without late penalties. Always confirm this with your HR department and Medicare before delaying enrollment.

What is the difference between Medicare and Medicaid for seniors?

Medicare is federal health insurance for seniors aged 65 and older based on age and work history. Medicaid is a state and federal program for people with limited income and assets. Some seniors qualify for both programs — they are called dual eligible — and can receive benefits from both Medicare and Medicaid simultaneously.

How does Medicare prescription drug coverage work for seniors?

Medicare drug coverage is provided through Part D plans sold by private insurance companies. Each plan has a formulary — a list of covered drugs. You pay a monthly premium, an annual deductible of up to $590, and then copayments for each prescription. The annual out-of-pocket maximum for Part D is $2,000 in 2026 — meaning you will never pay more than $2,000 per year for covered drugs.

How does Medicare Advantage work differently from Original Medicare for seniors?

Medicare Advantage is an alternative to Original Medicare provided by private insurance companies approved by Medicare. Instead of Medicare paying your claims directly the private insurer manages your coverage. You must use the plan’s network of doctors. Most plans include dental, vision, hearing and drug coverage. Plans have an annual out-of-pocket maximum which Original Medicare does not have.

When does Medicare coverage start for seniors?

If you enroll during the first 3 months of your Initial Enrollment Period your Medicare coverage starts the first day of your birthday month. If you enroll during your birthday month or the 3 months after your coverage start date is delayed by 1 to 3 months.

How does Medicare work for seniors who travel internationally?

Original Medicare generally does not cover healthcare received outside the United States except in very limited emergency situations near the US border. If you travel internationally a Medigap Plan C, D, F, G, M or N provides emergency foreign travel coverage up to $50,000 lifetime. Some Medicare Advantage plans also offer limited international emergency coverage. How Does Medicare Work for Seniors — Complete Guide 2026

Summary — How Does Medicare Work for Seniors?

How Does Medicare Work for Seniors — Complete Guide 2026 Medicare works by providing federally funded health insurance to Americans aged 65 and older through four main parts. Part A covers hospital care. Part B covers doctor visits and outpatient services. Part C or Medicare Advantage is an alternative all-in-one plan from private insurers. Part D covers prescription drugs.

Most seniors pay $185 per month for Part B in 2026 plus additional costs for drug coverage and any supplement plan they choose. Enrollment deadlines are strict and missing them results in permanent penalties.

The best way to understand exactly how Medicare works for your specific situation is to use the free plan finder at Medicare.gov or speak with a free SHIP counselor in your state.

This guide is for informational purposes only and is not medical or financial advice. Always verify current Medicare costs and plan details at Medicare.gov before making enrollment decisions. How Does Medicare Work for Seniors — Complete Guide 2026

Sources: Medicare.gov | CMS.gov | SSA.gov | AARP.org

How Does Medicare Work for Seniors — Complete Guide 2026

Last updated: April 2026 | Author: James Carter, Independent Medicare Research Analyst

7 Comments